We know the answer to success. If you want to get good at something you have to focus and do the work. Is this focus measurable in money management? Similarly, can we say something about manager focus through time? An interesting piece of new research looks at this problem in the paper, Diseconomies of scope and Mutual Fund Manager Performance.

This research finds that as the responsibilities of the manager become broader, there is a negative impact on alpha generation. There are diseconomies of scope which are different than just scale. The worst thing that can happen to a good fund manager in terms of alpha generation is that he is given more managerial responsibility. Good traders may not be good firm managers. The intensity or focus that may make someone a good fund manager falls when their scope of responsibilities is enhanced. A manager rewarded with more scope hurts fund investors.

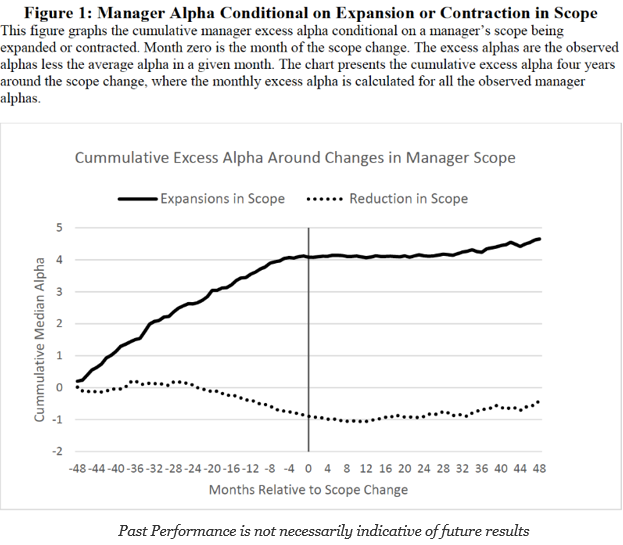

The paper measures alpha against changing expansion and contraction of scope for a broad set of mutual funds. Good alpha managers who are given increases in the scope of their responsibilities see a decline in their ability to generate more alpha. Those managers who have poorer alpha generation and have a cut in responsibilities or scope see an improvement in their ability to produce alpha. There are limitations with extrapolating the conclusions from this work and applying to hedge funds, but the intuition and basics results seem to be transferable.

Without making too broad a generalization, you don’t want a manager who goes out and gets a hobby or anything that takes away from a focus on alpha generation. You don’t want a manager who adds too many analysts and staff as he grows. You don’t want to use managers who have distractions from his core business. You do want managers who are focused and boring. A well-read global research or quant specialist is a positive. A renaissance man with many new interests who also manages his organization should not be a choice for investors.