“With a new secular bull trend, Commodities are among the most attractive markets this year. This commodity environment could be an exceptional moment to be in a spread program.”

The economic pendulum tends to be swinging towards commodities. The notion that low commodity prices are their own cure may be playing out in 2021[1], with help from its relationship to the post-pandemic economy and mean-reversion risks of a high dollar and U.S. stock market. Also, improving demand and central banks worldwide seeking expansionary policies are giving commodities a boost.

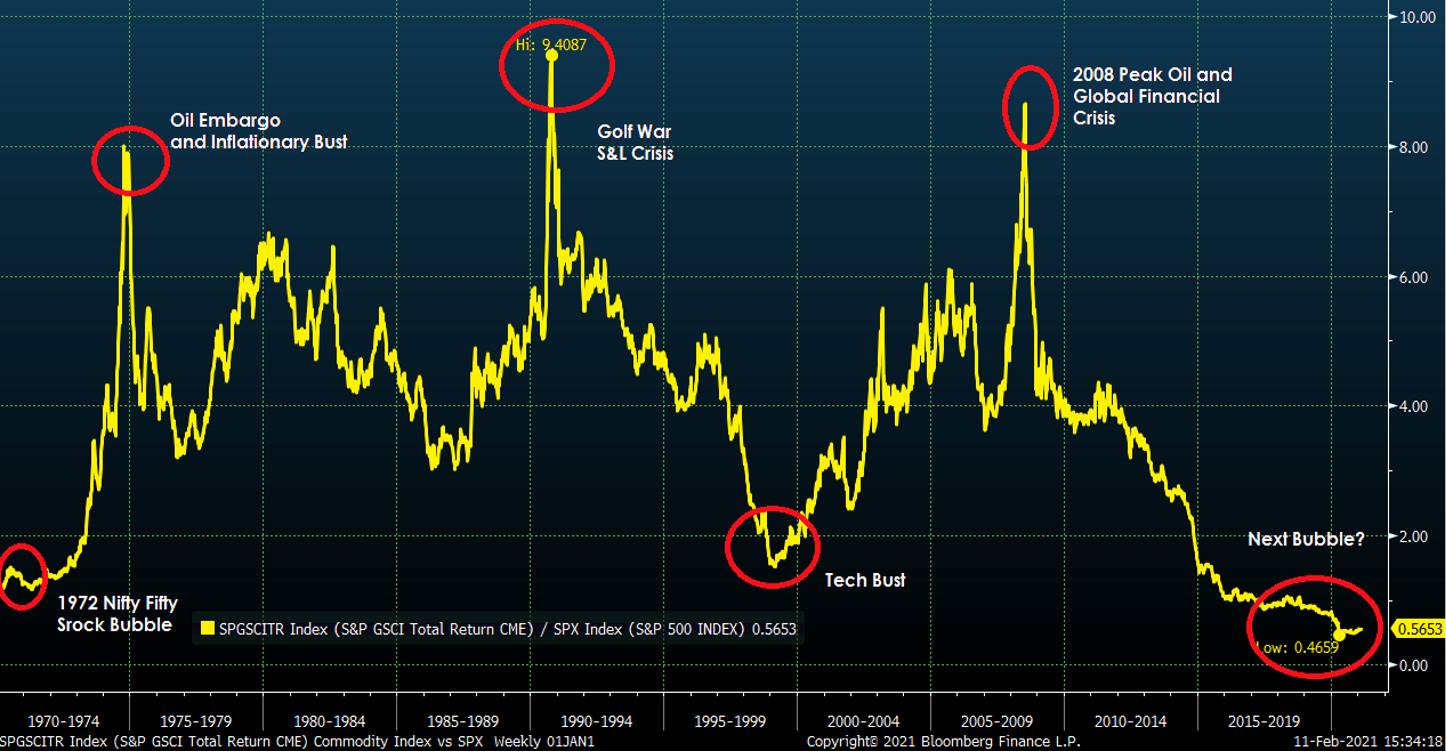

After years of a bear market, Commodities seem to be undervalued in relative terms (compared to equity and other markets) and in absolute terms as well. The Bloomberg Commodity Spot Index vs. the S&P 500 ratio is the lowest in decades and appears to have reached a bottom in March 2020.

Figure No 1 – S&P GSCI Total Return Commodity Index and S&P 500 Ratio making new lows

It is also important to note that the Bloomberg Commodity Index (BCOM) just broke its long-term bearish trend and, if that holds, could be the beginning of a secular trend in this market.

Figure No 2 – Bloomberg Commodity Index Log chart broke the long-term bear trend at the end of 2020.

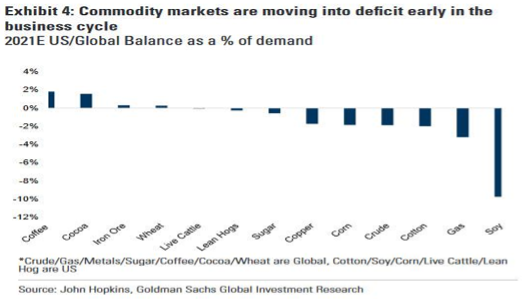

Additionally, almost all commodity markets are in or are moving towards a global deficit with inventories[2]. Such large-scale deficits are usually seen only late in the business cycle, underlining the unique environmental markets.

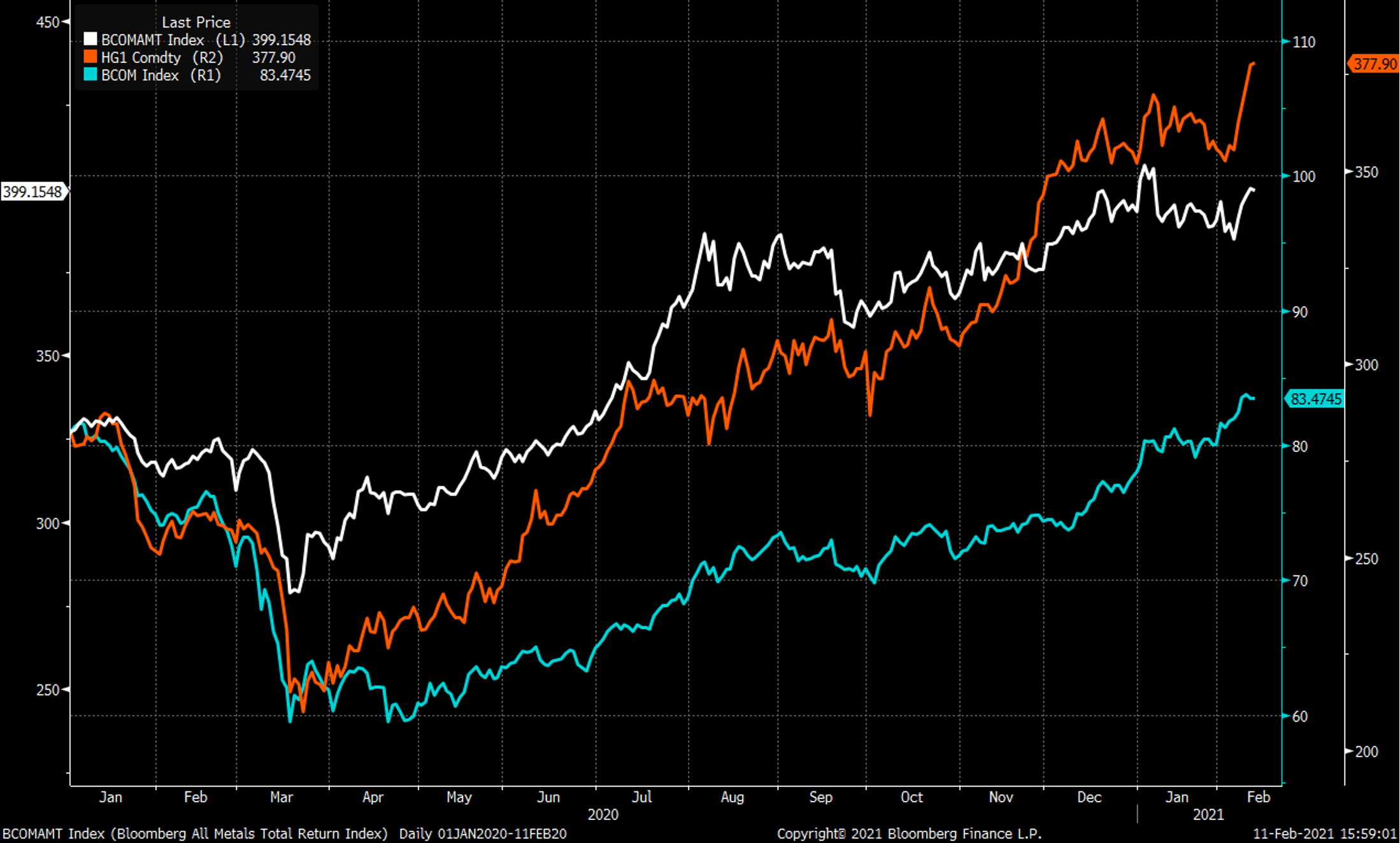

In metals, the new U.S. government could provide the most significant boost for metals. Industrial and base metals would be a substantial beneficiary of additional stimulus and infrastructure spending. Copper and nickel are on the demand side of the global economy’s electrification, and demand from global infrastructure could be higher than the Chinese demand cycle of 2006-2011. Copper may have some mean reversion after the Q4 2020/Jan 2021 rally, but there is still a long trend bull, and we do not expect this trend to change in 2021. The fundamentals and the technical favor Silver and Gold, even though a short-term correction may have taken place, the rally that started after the crash in March 2020, seems to persist. We won’t be surprised if the silver goes to $35-$40, boosted by increasing demand for electricity’s best conductor.

Bloomberg Metals Sub Index (BCOMAMT Index), Bloomberg Commodity Index (BCOM) and Copper Future Price

Grains seemed to reach a bottom in 2020, and since Q4 2020, prices have mainly recovered. Corn, soybean, and wheat are in backwardation, and, in our opinion, this may be a possible indication of the start of the bull market. U.S. grain exports, which are approaching multi-year highs as a percentage of supply, suggest that prices are more likely to continue the rebound. Some other factors are looking to favor the crops. For example, the U.S. corn belt has not seen an extreme dry weather year since 2012, when a weather occurrence happens on average every 7 years. In the case of soybeans, there is a heavy demand from China as the country needs food to feed and expand its hog inventories after the last years of swine flu, which affected supply. Although Brazil and Argentina seem to have enough stocks, a late start in South American crops can help raise soy prices, at least for the first quarter of 2021 when the US growing season starts. Grains can show a short-term price correction, but our view remains bullish in grains by observing the term structure. If a weather event occurs during this year, many inflows will follow this market, impacting the term structure of futures prices and providing possibilities for a spread program.

Bloomberg Grains SubIndex (BCOMGR Index)

Figure 4. Bloomberg grain subindex just broke its 100 and 200 moving average.

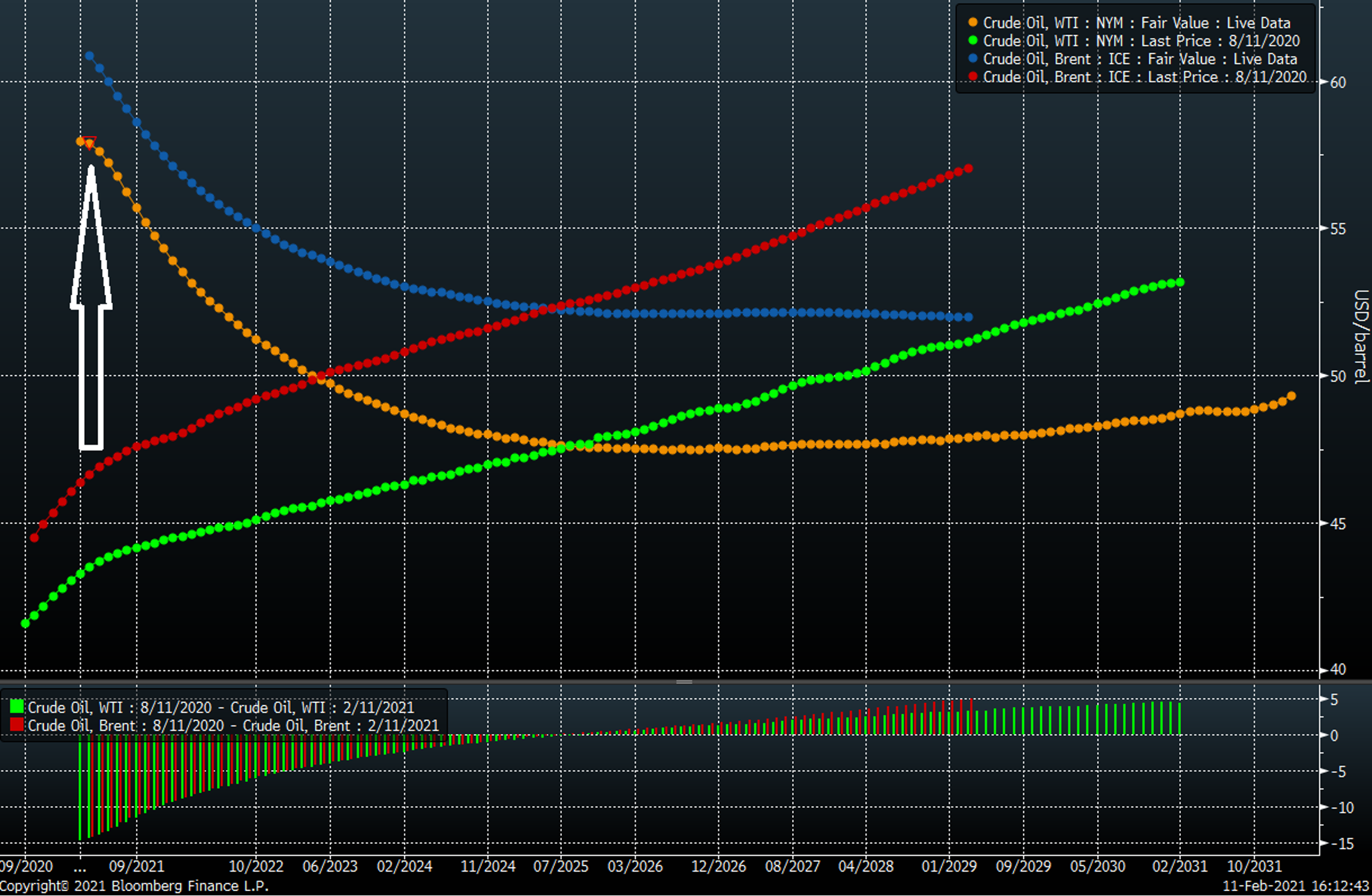

The new government agenda that prioritizes reducing carbon dioxide emissions and the ongoing innovation in green technologies, replacing fossil fuels for other energy sources, could affect oil and oil products demand. While crude oil is backward, we think it is because producers are hedging rather than a substantial increase in demand. After Saudi Arabia unexpectedly announced an additional 1 million barrels cut at the beginning of the year, WTI and Brent prices crossed above $50. While we do not expect an increase in demand in the mid-long term, a crude oil price above $60-$70 could mean more risk of a price drop than the start of a rally. We think natural gas prices are already being discounted in the forward curve to reflect the bearish fundamentals and that a more positive outlook appears in this market. The long-term viability of LNG exports and flows to Mexico while supply remains more restrained,[3] can fundamentally support natural gas prices in 2021. A weather event can distort calendar spreads where we are taking a close look at this market.

Brent and WTI Term Structure, actual vs. 6 months ago.

Figure No 5. WTI and Brent Oil actual term structure vs. 6 months ago, the forward curve moving from contango to backwardation.

Softs are also taking advantage of this rally with sugar and cotton, making multi-year record prices. Coffee and sugar could be beneficiaries of recovery in the Brazilian real. Simultaneously, some African governments’ policies and the confrontation between the cocoa producers and the big buyers will lead to high volatility of cocoa and fluctuations of spread prices in 2021. Those specific events create trading opportunities in calendar spread and relative value for us to profit.

HOW DOES SIGMA ADVANCED ANALYZE AND POSITION ITS PORTFOLIO TO TAKE ADVANTAGE OF THESE OPPORTUNITIES?

Sigma Advanced investment program aims to identify materially mispriced calendar and relative value spreads to generate non-correlated alpha by exploiting these inefficiencies on the term structure. When a new secular trend starts, a new inflow of money enters the market, and commodity prices begin to experience behavior seen before and never seen in history. For that reason, it is crucial for us to understand the market fundamentally but also quantitatively. First, we run several quantitative analyses to understand commodity price behavior in years where similar history occurred. That analysis includes stress tests, scenario analysis, and use of machine learning techniques. Secondly, we position the portfolio in line with our market view performing a balanced distribution of risk across all markets, and thirdly, we take tactical positions using advanced strategies in futures spreads to take advantage of the new environment and dislocation in prices that may occur.

Our portfolio remains diversified and risk-balanced across all sectors: energy, metals, grains, soft, and meats. Expecting a significant price shift in 2021, we remain confident that our disciplined, model-driven analysis and risk management approach will reward our investors.

About Sigma Advanced Capital Management:

Sigma Advanced Capital Management, LLC, an Illinois limited liability company, is a Commodity Trading Advisor registered with the Commodity Futures Trading Commission (CFTC) and a Member of the National Futures Association (NFA). Sigma Advanced specializes in commodity and carbon emission markets, seeking absolute returns across all economic cycles and market environments. It also seeks positive climate and social impact by supporting projects aligned with the Sustainability Goals ( SDGs) of 2030.

The company follows a Quant-Mental Investment process in futures, relative value, and calendar spread strategies, combining quantitative techniques such as statistical modeling, machine learning, natural language processing with discretionary and fundamental analysis.

Sigma Advanced Capital Management LLC currently managed two programs:

- The Global Advanced Futures and Spread Program (GAFS) – (QEP only): An absolute return program focusing on a risk-adjusted balanced portfolio of commodity calendar spreads, relative value strategies, and outright futures.

- Carbon Alpha Neutral Program (CNA) – (QEP Only): An Absolute return program focusing 100% on sustainable finance instruments, including carbon emission futures.

Portfolio Manager:

Carlos Arcila Barrera, CFA, CAIA, SCR is the founder and Portfolio Manager. Mr. Arcila, a Colombian National, has extensive experience in derivatives trading and risk modeling across a wide range of commodity and carbon emission markets, specializing in futures and spread strategies. He is the Adjunct Professor of Finance at Universidad de Los Andes and Associate Researcher for The Center of Sustainable Finance.

Carlos holds an MSc. in Finance from the University of Notre Dame (Magna cum Laude) and B.S in Business Administration from Universidad de Los Andes; he is a member of the International Association for Quantitative Finance (IAQF), and the American Finance Association (AFA), Carlos is a CFA Charterholder, CAIA Charterholder, Sustainable and Climate Change Risk (SCR) candidate and hold the Series 3 license.

Notes and Disclosures

DERIVATIVE TRANSACTIONS, INCLUDING FUTURES, ARE COMPLEX AND CARRY A RISK OF SUBSTANTIAL LOSSES. THEY ARE INTENDED FOR SOPHISTICATED INVESTORS WHO UNDERSTAND RISK. PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS

The information included within this document should not be copied, reproduced, redistributed, summarized, or otherwise shared or made public in part or whole without the prior written consent of Sigma Advanced Capital Management LLC and does not guarantee the accuracy, adequacy, or completeness of such information. References to specific securities, asset classes, and/or financial markets are only for illustrative purposes and are not intended to be recommendations. All investments involve risk, and investment recommendations will not always be profitable.

This material does not constitute investment, financial, legal, tax, or other advice; investment research or a product of any research department; an offer to sell, or the solicitation of an offer to purchase any security or interest in a fund; or a recommendation for any investment product or strategy. Past Performance Is Not Necessarily Indicative Of Future Results. The Risk Of Loss In Trading Futures And Options Can Be Substantial. Investors Should Carefully Review The Disclaimer at the end of this presentation. Nothing contained herein shall in any ways constitute any offer by Sigma Advanced Capital Management LLC to provide any service or product or an offer or solicitation to buy or sell any securities or other investment product opinions expressed herein are solely those of the author and are for general informational purposes only.

[1] McGlone Mike, Bloomberg Commodity Outlook – January 2021 Edition

[2] Goldman Sachs, Commodity Research Oct 2020

[3] Bloomberg Intelligence, Piazza US Nat Gas Commodity Research

Related Posts

Navigating Economic Crossroads: A Closer Look at the Unconventional Path

In the famous Robert Frost poem “The Road Not Taken,” two paths diverged, and he took the one less traveled. We can look at charts of the US economy and compare them to previous periods to see that so far, we are taking the less traveled path as well. It makes all the difference. Despite […]

Cargo Collapse Chronicles: Navigating the Economic Storm through Freight Industry Signals

Economists often look for the proverbial “canaries in the coal mine” to predict where we head next. Specific areas of the economy tend to presage slowing growth earlier than others. The shipping of materials from one place to another is one such area. A supply chain is either gearing up for future sales or reducing […]

Ag Market Update: Wheat Prices Drop, China Becomes Top Wheat Importer, and Soybean Complex Dynamics

Commentary provided by Chad Burlet of Third Street AG Investments For corn and soybeans, it was a quiet harvest month as far as prices were concerned. Futures contracts for both crops had only 5-7% trading ranges and settled within 1% of where they were a month ago. The U.S. harvest is progressing well, with both crops ahead […]