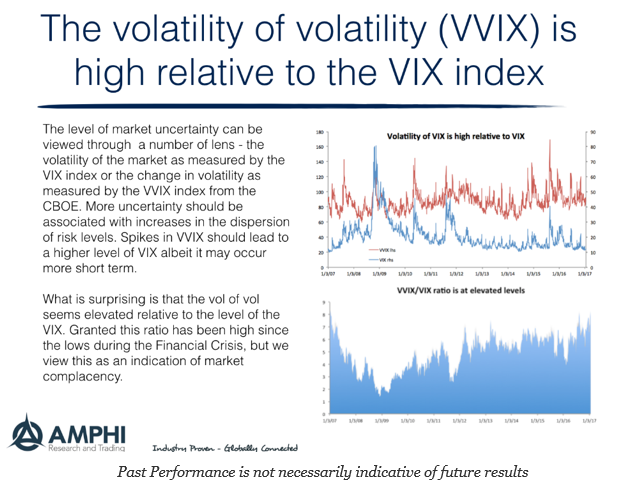

The VIX index is an effective measure of volatility expectations. The CBOE VVIX index measures the volatility of volatility for the VIX. If the volatility of volatility is increasing, there should be the expectation that volatility itself should also be increasing. We are seeing that the ratio of the VVIX to VIX is at high levels. Granted the VVIX index is off from recent highs, but the VIX index has continued to move lower even with the heightened policy uncertainty we have discussed in the past with our post on the one chart to look at for the new year.

Obviously when there is an elevated volatility ratio, it can return to normal through either a decline in the VVIX index or an increase in the VIX. Our view is that the change in US administration will continue to generate policy uncertainty as measured by the policy uncertainty index and thus the VIX should increase even if the volatility of volatility stays at current levels.

Related Posts

Anatomy of a Tough Month for Trend-Followers: Tariff Shocks & Volatility Spikes

It is often said that trend followers provide “crisis alpha.” This means that market stress often benefits their strategies. This follows logically as moves get larger, coordinate together, and run consistently, trading becomes easier. These managers quickly caution that they do not always provide this negative correlation. Price action can swing unpredictably against long-standing trends […]

Time-varying correlation – Diversification benefits are dynamic

What is the correlation between two assets? The correlation is critical because it is the driver for any diversification decision. The better question is, “What is the correlation now, and what can it be in the future?”. Correlations are often time varying and regime specific. In bad times, correlations rise, so the diversification expected is not present when you need it. This phenomenon requires more thinking about tail risks and how to best address them.

The “3 by 5 Index Card” on What You Need to Know About the February VIX Spike

University of Chicago professor Harold Pollack in an interview a few years ago mentioned that the best money advice can fit on a three-by-five inch index card. He was then challenged to write the card. His financial advice went viral. We follow this tradition by focusing on a simple “three-by-five index card” on the VIX volatility spike earlier the month.