Mark Rzepczynski, Author at IASG

Prior to co-founding AMPHI, Mark was the CEO of the fund group at FourWinds Capital Mgmt. Mark was also President and CIO at John W. Henry & Co., an iconic Commodity Trading Advisor. Mark has headed fixed income research at Fidelity Management and Research, served as senior economist for the CME, and as a finance professor at the Univ. of Houston Baer School of Business.

Changing the dynamics of enhanced cash – Switch from credit to alternative risk premia

Investors are always looking for ways to enhance cash returns – higher yield with liquidity and limited principal risk. The timing for using different enhanced cash techniques changes with market conditions. Widening the choice set through investing in alternative risk premia may be a way to meet enhanced cash goals without significantly increasing risk.

Mike Lombardi, football coaching and investing

I am not a football fanatic, but I picked up this book on a recommendation and was amazed by Lombardi’s insights on leadership and management. Mike Lombardi is long-time football executive and media analyst. The book focuses on Bill Belichick and the New England Patriots, but his conclusions could apply to any money management firm. A good money management firm is successful because it acts like a well-disciplined organization with a common purpose. That is no different than a competitively run sports organization. Lombardi finishes his book with five key recommendations for firm success that are worth presenting in bold.

“The Emeril Lagasse Theory” – Practical knowledge and culture is not often transferable

After hundreds of discussions with hedge fund managers, I am still surprised that there is a fear of revealing investment processes under the assumption that someone will steal their ideas and intellectual capital. There are few investment styles that are truly unique and special. What is special is still strategy execution – the practical process of delivering returns. Skill is with the decision-making execution of information and strategy.

From Hedge Funds to Passive Investing: The Need for a Paradigm Shift in Endowments

Endowments are supposed to be the smart money, yet if you review the recent exhaustive paper on return performance, you will get a different impression. Large endowments do better than small endowments, but when you compare with a simple 60/40 stock bond balanced fund, there is not a lot of alpha generated. See “Investment Returns and […]

Time-varying correlation – Diversification benefits are dynamic

What is the correlation between two assets? The correlation is critical because it is the driver for any diversification decision. The better question is, “What is the correlation now, and what can it be in the future?”. Correlations are often time varying and regime specific. In bad times, correlations rise, so the diversification expected is not present when you need it. This phenomenon requires more thinking about tail risks and how to best address them.

Behavioral economics – Is an atheoretical approach harmful?

Behavioral economics research has been path breaking and has truly impacted the thinking of most investors. Psychology is fundamental to human decision-making and our knowledge and understanding of economic agents has been enhanced through the large body of research in this area. Through finding exceptions and breaking down conventional utility maximization theory and wisdom, behavioral economic has advanced science, yet this work is not completely fulfilling. Our knowledge is filled with behavioral exceptions and leaves us with the impression that our decision-making skills are psychological damaged, but there is no unifying framework for how the range of biases fits within utility maximization, consumer behavior, market efficiency, and general decision-making.

Diverse ARP return pattern consistent with macro environment

A comparison of ARPs across asset classes and styles from the HFR indices shows consistency with the macro environment. We equalized the HFR ARP indices to a ten percent volatility for ease of discussion. April monthly returns are in grey while year to date returns are in red. The returns were generally lower than the market exposures, which were expected. The HFR numbers are averages and have shown significant dispersion. The low correlation across ARPs will create opportunities to improve the return to risk ratios through portfolio blending.

Microcosm versus Macrocosm – The impact of your mental model in decision-making

Every investor has a mental model of how the world works. Some may call this their philosophy. Other will call this their belief system. These mental models form their rational expectations or rational beliefs. They are rational because they are consistent with the mental model being employed. These beliefs should be unbiased. If they are not, it requires the investor to adjust their model to eliminate the bias.

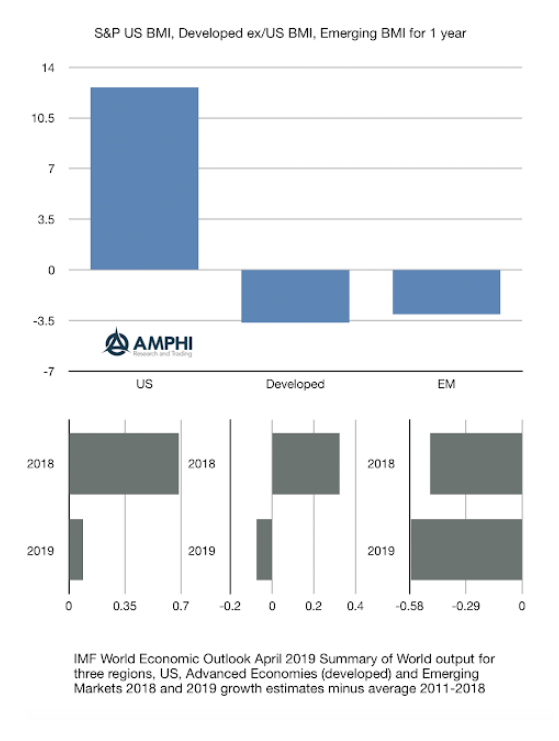

Global Macro Rationality and Equity Returns – Consistent With Growth Story

While some question the rationality of markets over the last few quarters, we believe equity markets are global macro consistent. This consistency can be seen in the return pattern for the US, developed markets, and emerging markets. As a simple surprise number, looked at the difference between the average growth rates for three macro categories from the IMF WEO from 2011-2018 against 2018 growth and expected 2019 growth.

A “Playbook” versus “Rulebook” and reaction to uncertainty

How do you deal with uncertainty? Some will suggest following rules. Disciplined and systematic investing is the best way to deal with the unknown because there is specific action regardless of the environment. Others argue for flexibility. Unknown or surprise events require special action. When faced with uncertainty, it may be best to adapt and adjust to the specific situation. Arguments can be made for both.

Credit risk – Profitability more important than leverage

There should be concerns about the amount of corporate leverage in the economy, but if there is no catalyst credit event, current risk is limited. We are not downplaying potential credit risk, but there needs to be focus on the right issues that will drive corporate bonds spreads higher.

Bending the return curve with rebalancing using trend-following

Rebalancing has become an essential tool for portfolio management. Nevertheless, market return patterns will affect the return impact of rebalancing. Regular rebalancing is a mean-reverting strategy. For example, suppose there is a simple 60/40 stock/bond portfolio. In that case, stronger stock performance will cause the allocation to deviate from the strategic allocation and lead to […]

How many animals should be in the factor zoo?

Investment factor growth has exploded to the point that are now close to 400 identified through research published leading finance journals. This factor explosion has been called the factor zoo and it is overcrowded. A careful review of the statistical testing procedures will tell us that it is highly unlikely that all of these identified factors will be true. Many are statistically significant only by chance given multiple testing problems. Additionally, if we impose transaction costs on these factors, their profitability will be diminished and in many cases not useful.