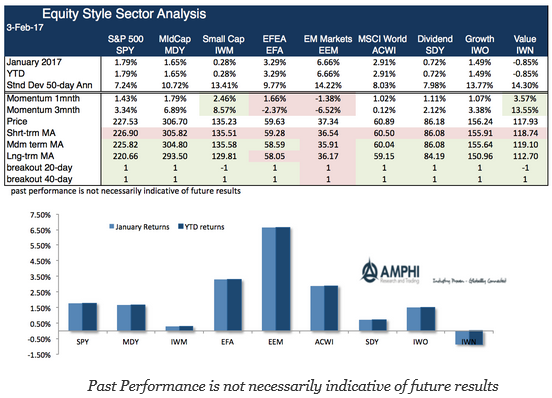

It was a positive month for risky assets, albeit more one of consolidation and than return break-out like what was seen last quester. Global markets outside of the US, especially emerging markets, showed large gains after a weak fourth quarter. The dollar gains post-election were partially reversed which added a tailwind to non-dollar investments of about 2%. After accounting for currency changes, developed non-dollar returns are back in-line with the US.

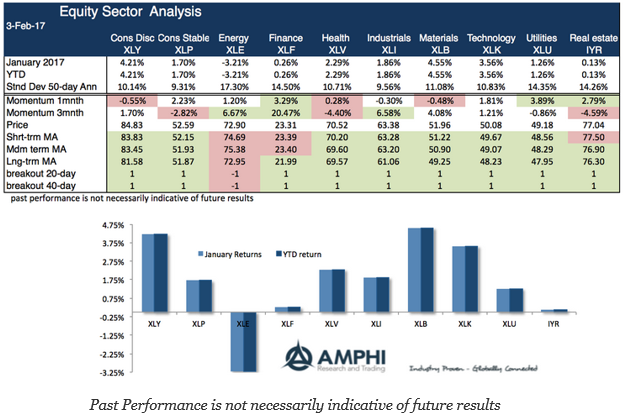

The oil sector reversed some of the strong gains over the prior to months as more range-bound oil and lower gas prices were discounted in these stocks. The largest gains were in materials and consumer discretionary which suggest an uptick in economic growth. Technology was also a strong sector winner while rate sensitive sectors showed only modest gains.

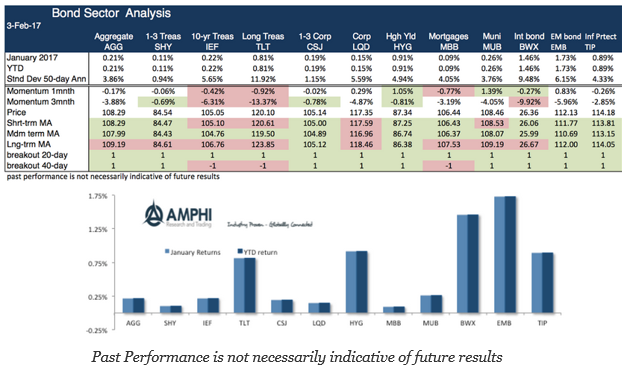

The bond sector was mostly flat for the month with the largest gains in non-dollar developed and emerging market bonds. However, these gains were related to the dollar decline which represented most of the return move.

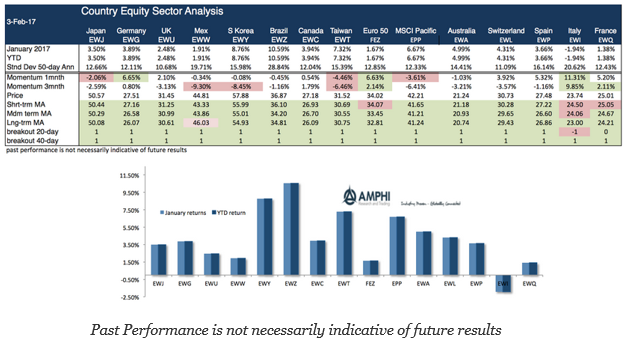

The country ETF sector showed the most variation with strong gains in Asian markets and Brazil. The weaker countries included Italy and France. Again, currency translation was a strong contributing factor.

After hundreds of discussions with hedge fund managers, I am still surprised that there is a fear of revealing investment processes under the assumption that someone will steal their ideas and intellectual capital. There are few investment styles that are truly unique and special. What is special is still strategy execution – the practical process of delivering returns. Skill is with the decision-making execution of information and strategy.

All hedge funds are not created equal as the return box chart shows for the post Financial Crisis period. There is a significant amount of dispersion across hedge fund styles. Over the period 2009-2018, the difference between the best and worst hedge fund category is almost 7 percent after we account for global equities and bonds.

The attraction to private equity and other less liquid alternatives is clear from the Guide to Alternatives by JP Morgan Asset Management. The return profile is much higher for private equity and debt funds than more liquid alternatives and global bonds; however, the dispersion in returns is multiples higher than what can be expected from other public categories.