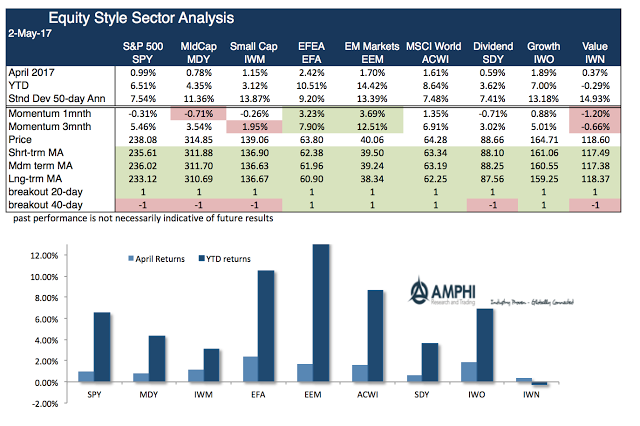

The positive equity performance for April and the strong year-to-date returns show that the risk-on environment continues. What is noticeable is the switch to global and emerging market gains although this has been helped by the declining dollar which may have added about one percent to performance. Performance has rotated from the reflation trade in the US to a broader investment in global equities.

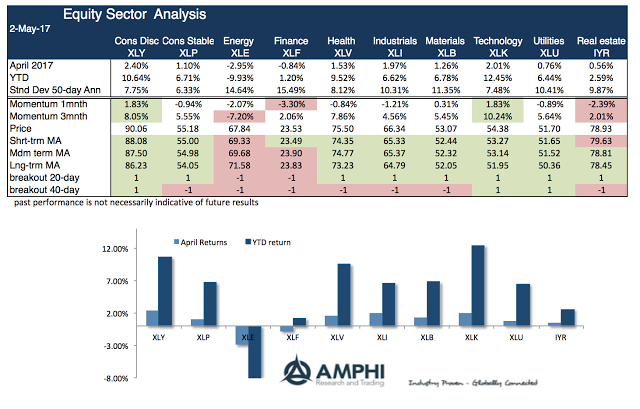

On a sector level, the year has not been positive for the energy sector which is down almost double digits. Finance is also having a difficult time this year based on regulation uncertainty and shifts in the yield curve. The technology and consumer discretionary sectors are both up double digits for the year. The gains in equities may be more concentrated than what many would expect if there is supposed to be stronger economic growth this year.

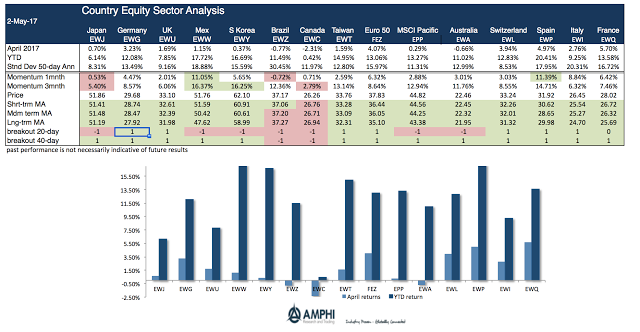

Many country equity indices are up over ten percent for the year with especially strong performance in countries that have strong export trade flows. Returns in Asian markets and Mexico have been stand-outs this year. The chance of a major trade war has diminished since the harsh talk at the end of the year.

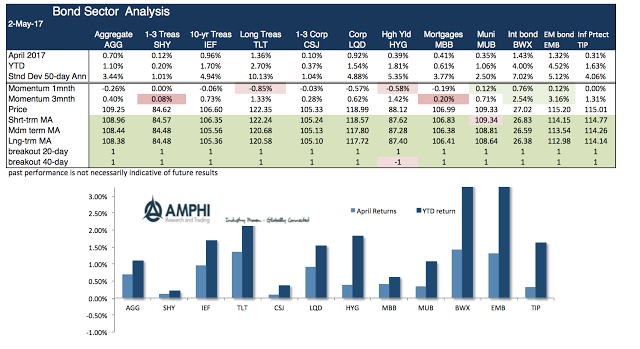

The bond sectors have shown much lower returns than equities, but that does not mean they have been return losers. Returns are consistent with a reflation trade. All sectors are positive for the year with the strongest gains in long duration and non-US bonds. Again, the decline in the dollar has been helpful for international bond investments.

We have been surprised with the continued strength in equity returns, but with a low volatility environment, good financial conditions, and a growth environment that is positive, it is hard to fight the trend. We are concerned about the gap between sentiment and real economic data, but at this point following trends is a reasonable strategy.