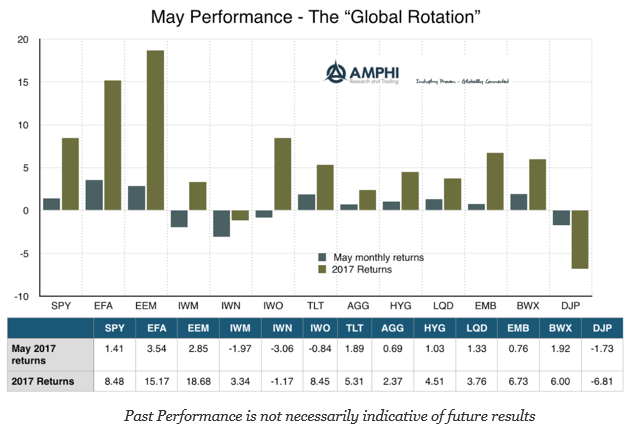

Call it the “Global Rotation”, but last month was a continuation of what we have seen for the year. There has been a flow of money into international stocks and increasing divergence between the rest of the globe and US risky assets. There is a dollar adjustment component to these returns, but there is no mistake that there is a preference for cheaper opportunities around the world.

Using a simple adjustment based on the DXY dollar index, the local returns should be moved down by over 2 percent which would have put returns closer to large cap US. The dollar has fallen about 5 percent since the beginning of the year which places global returns more in-line with large cap US. However, the switch from small cap and value in the US to other parts of the world is unmistakable along with the switch to large cap in the US.

Bonds posted strong gains both for duration and credit for the month. With a smaller probability of any inflation overshoot and monetary policy which seems to be measured, there is stronger demand for fixed income. This is more muted around the rest of the world after accounting for the move in the dollar. Commodities continue to slide and are the asset class laggard.

After hundreds of discussions with hedge fund managers, I am still surprised that there is a fear of revealing investment processes under the assumption that someone will steal their ideas and intellectual capital. There are few investment styles that are truly unique and special. What is special is still strategy execution – the practical process of delivering returns. Skill is with the decision-making execution of information and strategy.

All hedge funds are not created equal as the return box chart shows for the post Financial Crisis period. There is a significant amount of dispersion across hedge fund styles. Over the period 2009-2018, the difference between the best and worst hedge fund category is almost 7 percent after we account for global equities and bonds.

The attraction to private equity and other less liquid alternatives is clear from the Guide to Alternatives by JP Morgan Asset Management. The return profile is much higher for private equity and debt funds than more liquid alternatives and global bonds; however, the dispersion in returns is multiples higher than what can be expected from other public categories.