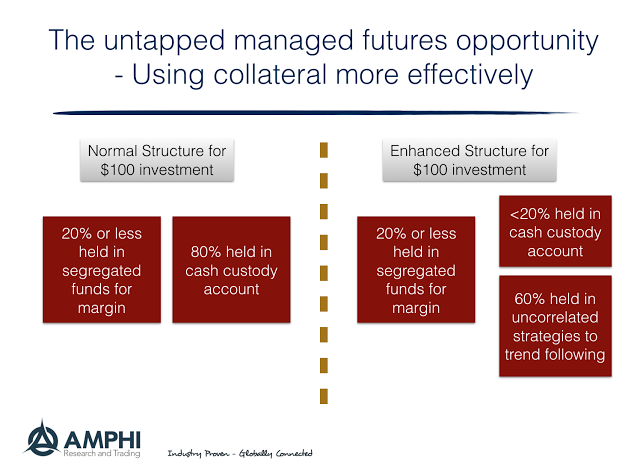

Managed futures investments have the key structural feature that they do not use leverage in the sense of borrowing money to increase notional positions relative to cash. In most cases, margin requirements are a small fraction of the capital invested in a program or fund. A managed futures fund may only use less than 20 cents on the dollar for margin while 80 cents or more may be held in a custody account at close to zero interest rate. Nevertheless, some managers are more aggressive and may hold funds in an enhanced money fund or short-term bond fund to add to return. Of course, some investor will use a separate account and only provide funds for margin with a cushion. This cuts the excess cash held by the manager.

Generally, capital is not used efficiently with this hedge fund strategy. By efficiency we mean that returns can be enhanced by deploying more of the money in the fund in investments that have a return higher than cash. This will have an impact on overall volatility, but this can be managed to still target a specific volatility level for the fund.

A simple way of more efficiently using the capital is to employ managed futures as a overlay program so that all of a portfolio’s capital is used to generated the highest returns possible. The notional trading size of the overall portfolio will be higher, but the volatility of the overall portfolio can still be managed to specific volatility target.

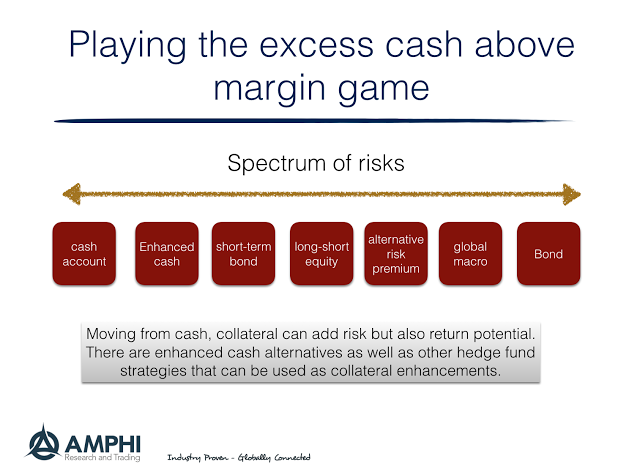

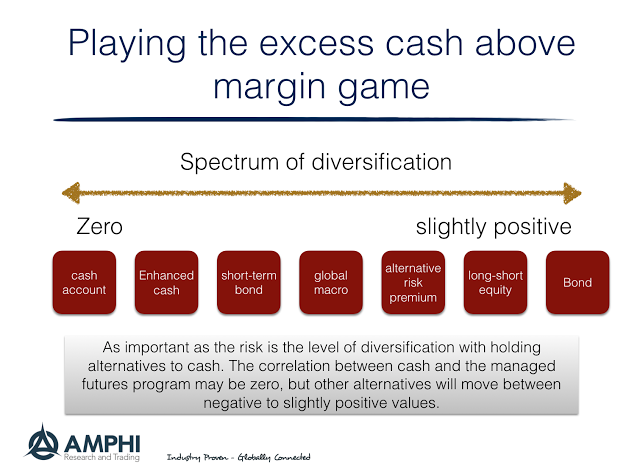

There is both potential benefits and costs with using the capital that is held in cash based on the correlation between the managed futures program and the choice of investment for the non-margin funds. If the funds are held in an asset or strategy that has higher volatility than cash, the net result may be an increase in the overall volatility of the fund. The portfolio volatility will be based on the combination of the volatility for the cash component and the correlation with the futures program. An investor may not want to pay for the higher volatility or return that is not associated with this use of the cash; however, that is an issue of negotiation between the manager and the investors.

The cash component decision can be thought of as a continuum of risk and return with the base position being cash which has no correlation with the managed futures returns and has limited or no return. The manager or investor can move out the risk spectrum for the collateral usage. However, the impact on overall volatility will be related to the correlation between the collateral account and the managed futures program. If there is a negative correlation, the enhanced collateral may actually reduce overall program risk.

The choice set of how to employ managed futures and efficiently use capital is fairly broad but can help widen the return opportunities for both manager and investor. Holding cash may be the best alternative but that decision should be made after looking at all of the choices for excess collateral.