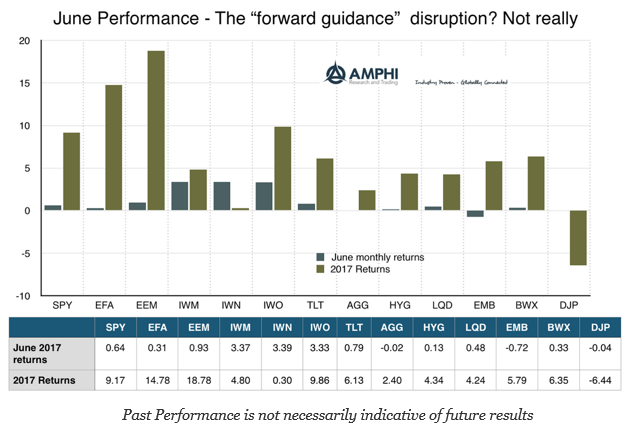

In spite of the market anxiety during the last week of the month, most major indices generated positive returns for June. The only exceptions were the emerging market bond index (EMB), the Bloomberg commodities index (DJP) and the Barclays Aggregate index (AGG). It was surprising that small cap, value and growth all posted strong gains after falling behind global and large cap equities. Bonds were generally positive even with the turbulence in the last week.

The S&P 500 index was more volatile given the back and forth of 1% move days. The market has not seen this type of volatility in 2017. There were major jumps in the VIX index which has been exceptional calm over the last six weeks. The bond index (TLT) fell about three percent in the last week of the month yet it still generated a gain for the month. The bond decline was driven by the belief that ECB tapering may begin sooner than expected. This was based on a speech from ECB President Draghi which was “clarified” the next day. In general, there is a growing pessimism in bond markets that a cut in liquidity will negatively affect portfolio balances. Earlier in the month bonds rallied on the view that growth and inflation would be lower than expected.

While not demonstrated in monthly performance, we see a very uncertain bond market that is vacillating between growth and inflation concerns and a view that a tapering of central bank policies will have a negative impact on supply even if necessary for normalization. Equities are responding to an end of the Trump trade coupled with high valuations. Exhaustion of the same old investment stories leads to conservative behavior. This is likely to show itself through the summer.