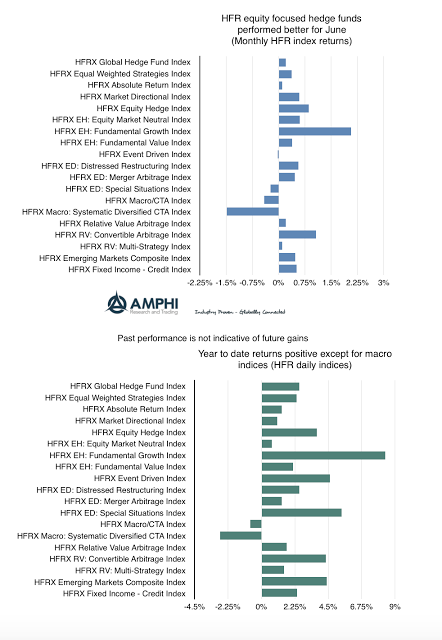

The equity focused HFR hedge fund indices produced positive returns for the month of June while those indices focused on broad-based macro trades declined. Equity focused hedge fund managers will often do better when there is more dispersion across industry sectors and when there is stronger performance in broader-based indices like the Russell 2000. The market saw strong gains in both growth and value indices and less emphasis on large cap names. The fall in tech stocks which have been at elevated levels may also have been a contributor to some hedge fund gains.

The half year numbers for hedge fund styles are generally positive except for the macro strategies which have not been able to find profitable opportunities. The reversal in bond trends in June and a lack of connectedness between macro fundamentals and market behavior has hurt these strategies.

The larger question is whether these numbers are consistent with investor expectations. Versus a small cap or value index, hedge fund managers, on average, may be finding profitable opportunities at lower risk. Against global equity indices, the answer is less supportive. Most will view a comparison of hedge fund styles against broader indices as suspect, but investors still have to make asset allocation decisions and one of the core questions to be answered is whether to emphasize beta or alpha. To address this issue, alpha and beta generators have to be compared. Of course, the time horizon for comparison is critical but performance analysis is a core issue at quarter-end. What action is to be taken is a more complex, but measurement and comparison are necessary and will be done. By a number of measures, investors may feel hopeful but mixed by 2017 average performance.