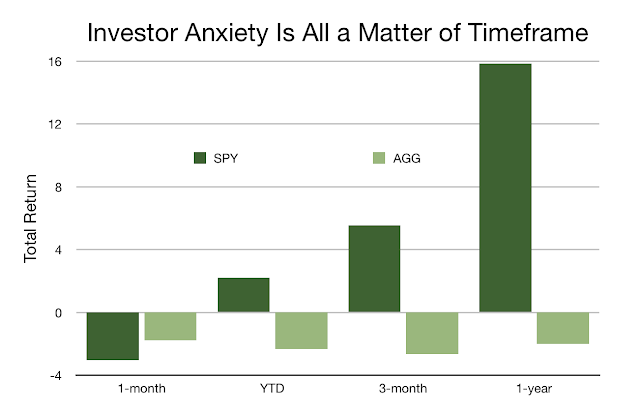

How would you feel about your investment portfolio if you went to sleep at the beginning of the year and woke-up on Friday? What if you stuck your portfolio in a drawer and pulled it out after three months or a year to look at performance? My guess you would say you were happy and comfortable with your investment decisions, yet there has been a lot of investor anxiety this month.

The recent sell-off is vivid in our minds. Many have compared this event with some of their worst investment months in their lives, yet over a longer timeframe the events of February may not matter. Our investment anxiety should be proportional to the rebalancing period we use and the time horizon of the investment. We are not saying that the repricing of risk should be ignored but rather it should be placed in the context of portfolio objectives, past performance, and investment horizons.

After hundreds of discussions with hedge fund managers, I am still surprised that there is a fear of revealing investment processes under the assumption that someone will steal their ideas and intellectual capital. There are few investment styles that are truly unique and special. What is special is still strategy execution – the practical process of delivering returns. Skill is with the decision-making execution of information and strategy.

All hedge funds are not created equal as the return box chart shows for the post Financial Crisis period. There is a significant amount of dispersion across hedge fund styles. Over the period 2009-2018, the difference between the best and worst hedge fund category is almost 7 percent after we account for global equities and bonds.

The attraction to private equity and other less liquid alternatives is clear from the Guide to Alternatives by JP Morgan Asset Management. The return profile is much higher for private equity and debt funds than more liquid alternatives and global bonds; however, the dispersion in returns is multiples higher than what can be expected from other public categories.