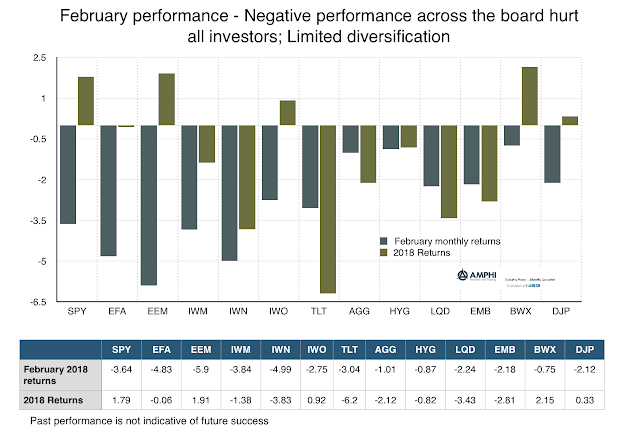

February was a bad month for investment performance. All of the major ETF indices we normally follow were negative. Diversification was an elusive concept and reinforced the key portfolio allocation risks of rising correlation. There is no positive spin with these numbers other than less risky assets like bonds fell less than more risky assets, although year to date numbers show that bonds have not been a safe haven. There are a few takeaways from the month:

- When there is a major financial shock, correlations move to one and there is no hiding from risks.

- “Hedges” based on statistical correlation were far from perfect over the short-run. While structured hedges like options will do better when there is a short-term shock, they are more expensive in the long-run.

- Financial shocks without fundamental context will see relatively quick reversals; perhaps not a full 100%, but endogenous shocks get reversed.

- The monthly move for the SPY was within the context of expectations when annualized vols were converted to monthly moves. The monthly equity decline was more than one standard deviation for a 10% volatility but less than one standard deviation for a 20% volatility.

- The market has now repriced volatility to about double what is was at the beginning of the year.

- The short vol bias embedded in markets is real and still exists.

The key takeaway is that the calm markets of 2017 will not be the norm for 2018. A volatility environment of around 20% for the VIX is higher than the long-term average of 15% since its inception and tells us that we should be prepared for greater daily and monthly moves.