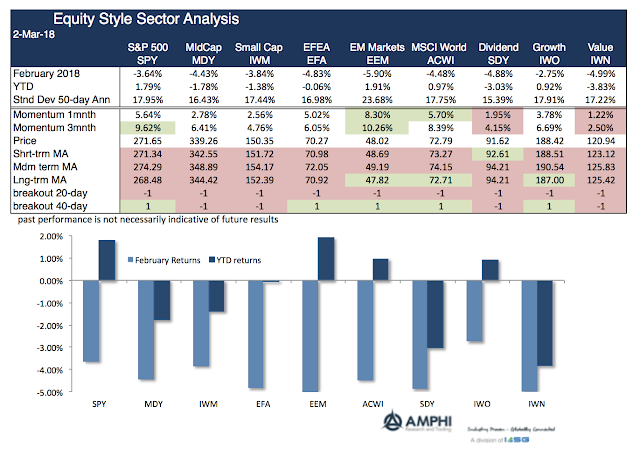

There is little protection for investors when there is a price revaluation from a volatility shock. All equities styles declined in February. All equity sectors generated negative returns. Country equity returns were negative and bonds offered no protection. Correlations all moved higher in February although there are some interesting limited opportunities. A comparison of momentum from the prior month and three-month period show the strength of the reversals. Prices fell below short, medium and long-term trends except for few outliers.

Nevertheless, a number of styles are now above 40-day breakout levels. Emerging markets, growth, and the world ETF were still above long-term averages (80-day) at the end of February.

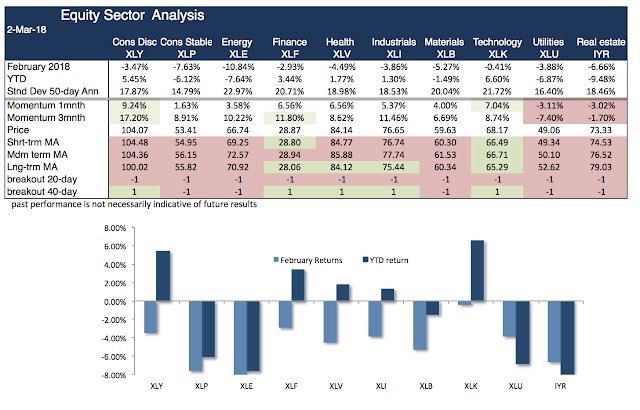

Sector performance was negative across the board, but the technology sector is still above multiple moving averages. Other sectors that are performing better than longer-term moving averages are finance, health, and industrials.

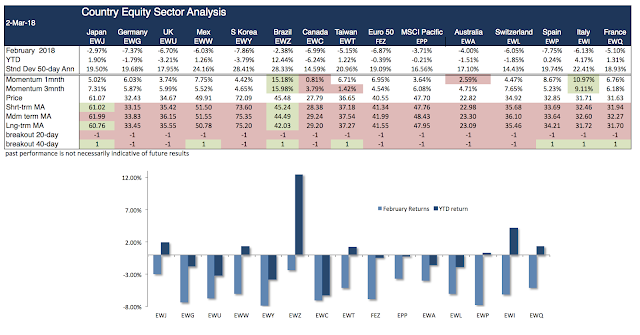

Sovereign equity sector analysis shows the decline was across the globe. No country index was unaffected. However, Brazil equities have done well year-to-date and Japan equities are still above short-term and long-term moving averages.

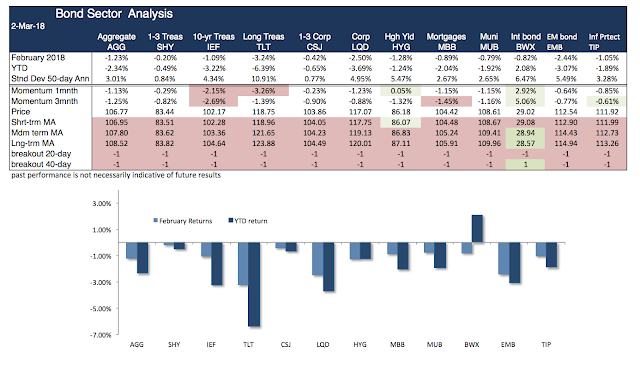

Bond markets only offered limited protections through more muted loses. Even short-term corporates generated negative returns. International bonds have generated positive year-to-date returns because of the fall in the dollar. All these bonds sectors are below moving averages except for international bonds.

The VIX index moved from 10% to a spike of 40% and then settled at a 20% level. To attract new capital, prices for risky assets have had to fall. Markets moved higher on the reversal from 40% to 20% for the VIX, but March is a new month which will react to new forward information in a more volatile information. Without good news in growth or earnings, there may be limited reason to see higher valuations.