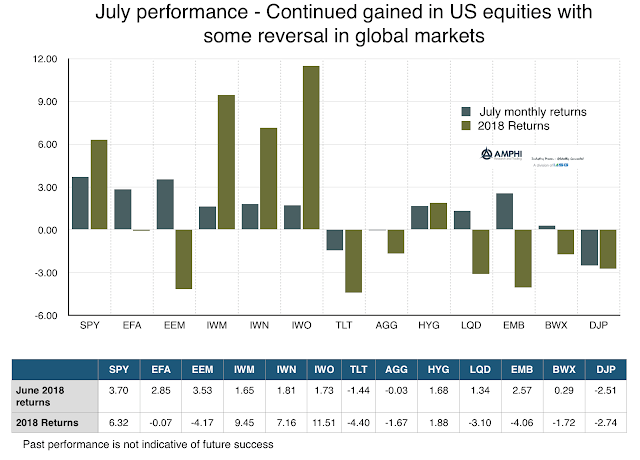

First look at the data to see what weighted market opinion is telling us. July marks a reversal to more risk-on behavior with strong gains in large cap US stocks as well as international and emerging market equities. While small cap, growth, and value indices all did well, the broader international concerns affecting risk behavior have abated. This positive global view was also seen in the international bond markets. The dollar rise from a desire for safety was contained and more range bound. Along with international bonds, credit markets improved with tightening spreads. The only losers for the bond sector were long-duration Treasuries and commodities.

Away from the headline grabbing FAANG stocks, the markets have responded to the higher economic growth story which culminated with a 4% second quarter growth announcement. The combination of continued good economic news and a dampening of trade war rhetoric led to a more hopeful market. While trade war discussions with China are still a market focus, the news with the EU is more suggestive of compromise or even a new trade deal with better terms. Of course, these trade discussions almost always exclude autos and agriculture which are industries that hold special appeal by the EU.

While the link between economic growth and equity prices is not always definitive, we can say that the announcements of tech firms like Facebook, Netflix, or Twitter do not represent signals for where earnings will go for the average firm. The growth story and its impact on wages and inflation will still be the key driver for the rest of 2018.

Related Posts

Navigating Economic Crossroads: A Closer Look at the Unconventional Path

In the famous Robert Frost poem “The Road Not Taken,” two paths diverged, and he took the one less traveled. We can look at charts of the US economy and compare them to previous periods to see that so far, we are taking the less traveled path as well. It makes all the difference. Despite […]

Cargo Collapse Chronicles: Navigating the Economic Storm through Freight Industry Signals

Economists often look for the proverbial “canaries in the coal mine” to predict where we head next. Specific areas of the economy tend to presage slowing growth earlier than others. The shipping of materials from one place to another is one such area. A supply chain is either gearing up for future sales or reducing […]

Ag Market Update: Wheat Prices Drop, China Becomes Top Wheat Importer, and Soybean Complex Dynamics

Commentary provided by Chad Burlet of Third Street AG Investments For corn and soybeans, it was a quiet harvest month as far as prices were concerned. Futures contracts for both crops had only 5-7% trading ranges and settled within 1% of where they were a month ago. The U.S. harvest is progressing well, with both crops ahead […]