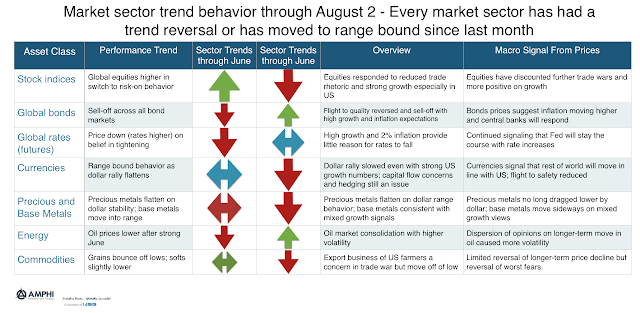

Our tracking models for the end of July show that there have been changes in direction for all major sectors. This would usually suggest significant loses for trend managers but the relatively mild volatility and the slow reversals allowed for adjustment of signals to mitigate loses.

Equity indices moved higher around globe while bonds reversed and sold-off. Between good economic numbers and the worst fears not being realized, the market moved to risk-on positioning. Rates suggest that quantitative tightening will continue. The dollar rally slowed which cause precious metals to move sideways. The energy rally also slowed albeit there is a large dispersion in market views. Commodity markets were mixed but the strong grain price declines in June have started to reverse, but soft prices are trending lower.

Given the sector reversals between June and July, it is hard to say what will be the potential winners for August. With vacations for many this month, position changes will be limited without a major economic surprise.

Related Posts

Navigating Economic Crossroads: A Closer Look at the Unconventional Path

In the famous Robert Frost poem “The Road Not Taken,” two paths diverged, and he took the one less traveled. We can look at charts of the US economy and compare them to previous periods to see that so far, we are taking the less traveled path as well. It makes all the difference. Despite […]

Cargo Collapse Chronicles: Navigating the Economic Storm through Freight Industry Signals

Economists often look for the proverbial “canaries in the coal mine” to predict where we head next. Specific areas of the economy tend to presage slowing growth earlier than others. The shipping of materials from one place to another is one such area. A supply chain is either gearing up for future sales or reducing […]

Ag Market Update: Wheat Prices Drop, China Becomes Top Wheat Importer, and Soybean Complex Dynamics

Commentary provided by Chad Burlet of Third Street AG Investments For corn and soybeans, it was a quiet harvest month as far as prices were concerned. Futures contracts for both crops had only 5-7% trading ranges and settled within 1% of where they were a month ago. The U.S. harvest is progressing well, with both crops ahead […]