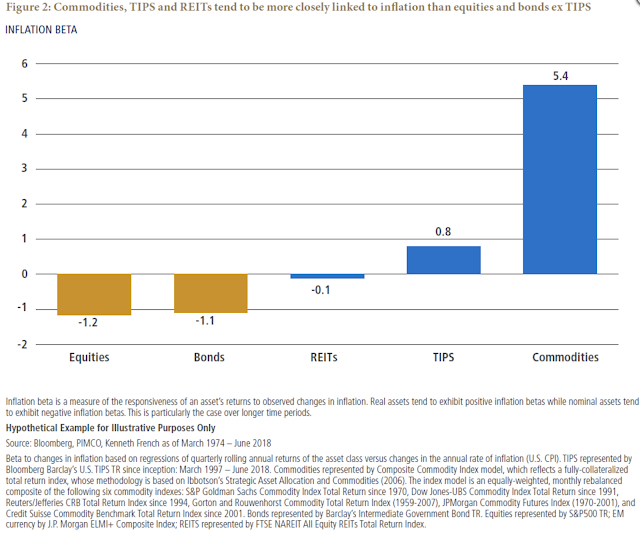

There is a correlation between commodity investing and inflation. Commodities do well late in the business cycle when bonds usually underperform, and inflation is heightened. Research work by PIMCO measures the inflation beta for some significant asset classes. Stocks have a negative inflation beta even though earnings should rise with inflation. Bonds as nominal assets show a strong negative beta. Real estate, which should be a real asset, is neutral to inflation. TIPS has a beta close to one, which is consistent with the underlying construction of the security. Commodities have a very large inflation beta that can be used to take advantage of inflation concerns. Still, this high inflation beta may be a concern for some investors.

Implications of High Inflation Beta

Thinking holistically, a large inflation beta means that a minor allocation change may be necessary to offset inflation risk in other parts of the portfolio and generate the right global outcome. However, this means that any sector bet tied to commodity beta indices is highly exposed to inflation risk. If the higher inflation never materializes, investors may be overexposed to this inflation beta and see strong commodity underperformance. This is a classic problem of thinking about risk at the portfolio versus asset class level. Portfolio risk should be the focus, but investors are not immune to scrutiny at the sector level.

Adjusting Inflation Beta

The inflation beta can be adjusted by changing the exposure to commodities, or it can be restructured or blended through exposure to alternative risk premia that look to commodities for strategy but not directional commodity risk. Alternative risk premia in carry, value, momentum, or volatility can allow investors to take advantage of the changing dynamics in commodities without pure directional and inflation beta risk. For example, a combination of beta risk and risk premium exposures can smooth returns while still allowing for controlled inflation exposure.

Rethinking Portfolio Risk During Inflation

A potential increase in inflation is a good time to rethink the factor risk exposures in a portfolio. First, what is the current inflation beta for the portfolio? Second, what is the desired inflation portfolio beta? Third, how is that inflation beta going to be achieved? While inflation is at or above the 2% target in the US, it is still not too late to think about the right inflation beta for a portfolio.

Photo by Martin Sanchez on Unsplash

Related Posts

Race to Nowhere: Markets Pause Before the Next Big Move

Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere. As of mid-February, the S&P 500 is […]

Systematic vs. Discretionary Trading: Which Strategy Is Right for Your Portfolio?

Investors face many choices when selecting investments. Historically, the main divide was between fundamental and technical trading. The growth of computer systems for trading has introduced a potentially larger variable that will only increase as AI advances, whether in systematic (rules-based) or discretionary (human judgment) trading. In just my 20 years working in the industry, […]

The Evolution of Trading from Systematic to AI

Is AI the next step in the evolution of trading? History proves new tools storm the markets, then high adoption erases their edge. What can futures trading history teach us about AI’s trajectory? The 1980s: Rise of Rules-Based Trading Building on simple regression models that aimed to identify patterns across sectors, the 1980s showed that […]