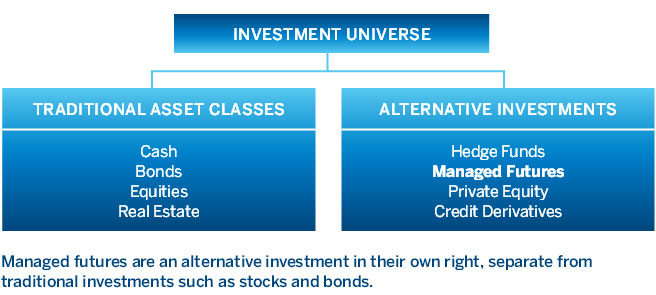

WHAT ARE MANAGED FUTURES?

The term managed futures describes a diverse subset of active hedge fund strategies that trade liquid, transparent, centrally-cleared exchange-traded products, and deep interbank foreign exchange markets. Managers in this sector are called commodity trading advisors (CTAs) and their strategies are largely focused on financial futures markets with additional allocations to energy, metals and agricultural markets.

For the purposes of this booklet, managed futures do not include futures accounts where futures are used in risk-management programs or hedge funds. Those funds may be used to dynamically adjust the duration of a bond portfolio or to hedge the currency exposure of a foreign equity portfolio.

Managed futures have been used successfully by investment management professionals for more than 30 years. Institutional investors looking to maximize portfolio exposure continue to increase their use of managed futures as an integral component of a well-diversified portfolio. With the ability to go both long and short, managed futures are highly flexible financial instruments with the potential to profit from rising and falling markets. Moreover, managed futures funds have limited correlation to traditional asset classes, enabling them to provide the opportunity for enhanced returns and lower overall volatility.

Growth over the past decade in managed futures has been substantial. In 2002, it was estimated that more than $45 billion was under management by managed futures trading advisors which increased to $334 billion by the end of the second quarter in 2012.

BENEFITS OF MANAGED FUTURES

By their very nature, managed futures provide a diversified investment opportunity. Trading advisors can participate in more than 150 global markets; from grains and gold to currencies and stock indices. Many funds further diversify by using several trading advisors with different trading approaches.

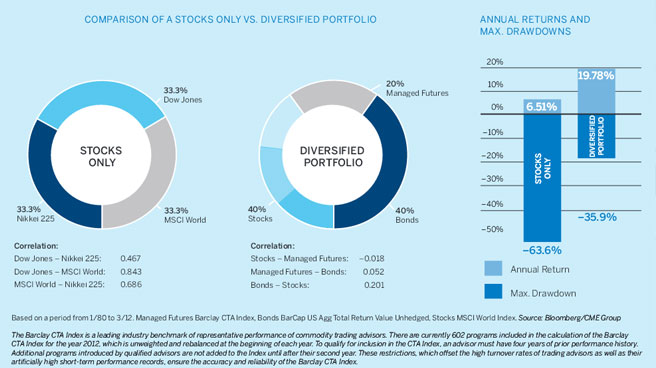

In this example below, the overall risk (as measured by maximum drawdowns) is reduced from -63.6% to -35.9% and the return increases from 6.51% to 19.78%. This is mainly due to the lack of correlation and, in some cases, negative correlation between come of the portfolio components in the diversified portfolio. There is even negative correlation between stocks and managed futures in this example, as the two markets move independently from each other.

The benefits of managed futures within a well-balanced portfolio include:

- Potential to lower overall portfolio risk

- Opportunity to enhance overall portfolio returns

- Broad diversification opportunities

- Opportunity to profit in a variety of economic environments

- Limited losses due to a combination of flexibility and discipline

1. POTENTIAL TO LOWER OVERALL PORTFOLIO RISK

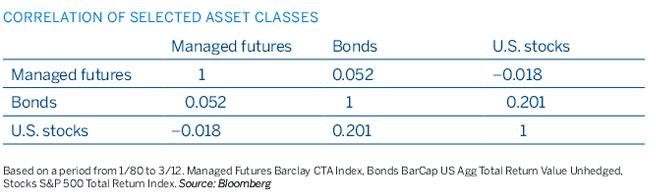

The main benefit of adding managed futures to a balanced portfolio is the potential to decrease portfolio volatility. Risk reduction is possible because managed futures can trade across a wide range of global markets that have limited long-term correlation to most traditional asset classes. Moreover, managed futures funds have historically performed well during adverse economic or market conditions for stocks and bonds, thereby providing excellent downside protection in most portfolios.

One of the tenets of modern portfolio theory, as developed by Nobel prize-winning economist Professor Harry M. Markowitz, is that more efficient investment portfolios can be created by diversifying among asset classes with low to negative correlations. Adding a managed futures fund to a portfolio of traditional stocks and bonds has the potential to reduce risk and improve performance.

2. OPPORTUNITY TO ENHANCE OVERALL PORTFOLIO RETURNS

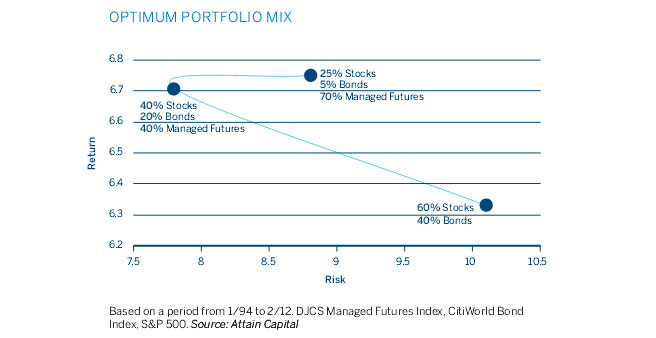

A portfolio that includes managed futures, historically, would have provided higher returns and lower risk than one without managed futures at all. In this Efficient Frontier example, the addition of managed futures to the typical stock and bond portfolio increases the annual rate of return, while lowering the volatility of the portfolio. There is a point of diminishing returns, and the curve can help find maximum efficiency. In this case, the data from 1994 to February 2012 sees the optimal portfolio for the highest return at the lowest risk level to be 40% stocks, 40% managed futures, and 20% bonds. There’s no guarantee that this curve will look the same five years from now, or even a year from now. And the Efficient Frontier has a flaw in that it considers only volatility when assessing risk when there are other factors to be considered.

3. BROAD DIVERSIFICATION OPPORTUNITIES

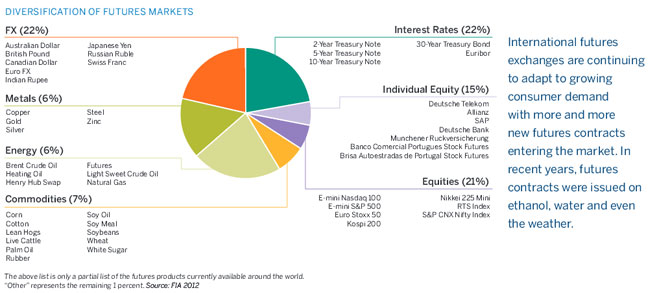

MANY DIFFERENT FUTURES MARKETS

Managed futures are highly flexible and traded on many regulated financial and commodity markets around the world. By broadly diversifying across global markets, managed futures can simultaneously profit from price changes in stock, bond, currency and money markets, as well as from diverse commodity markets having limited correlation to traditional asset classes.

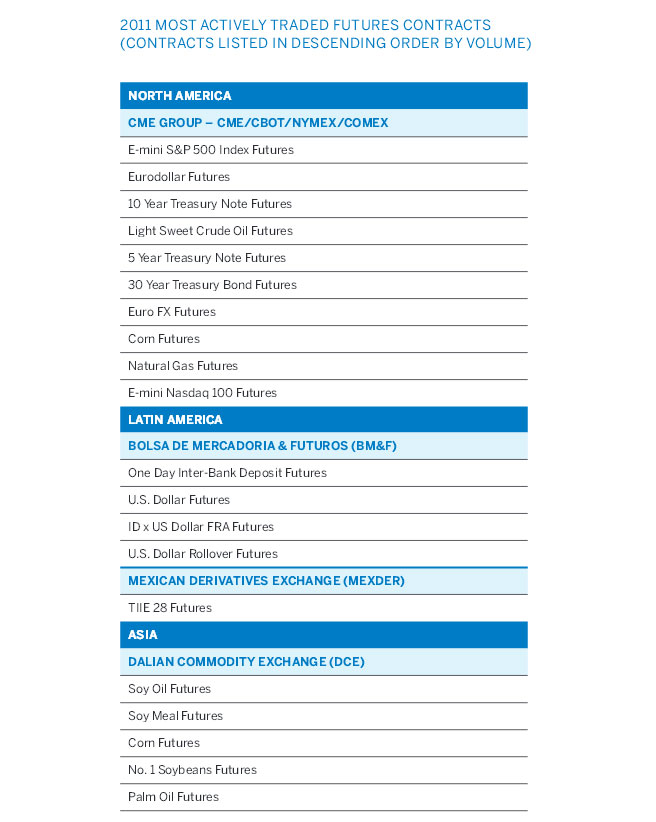

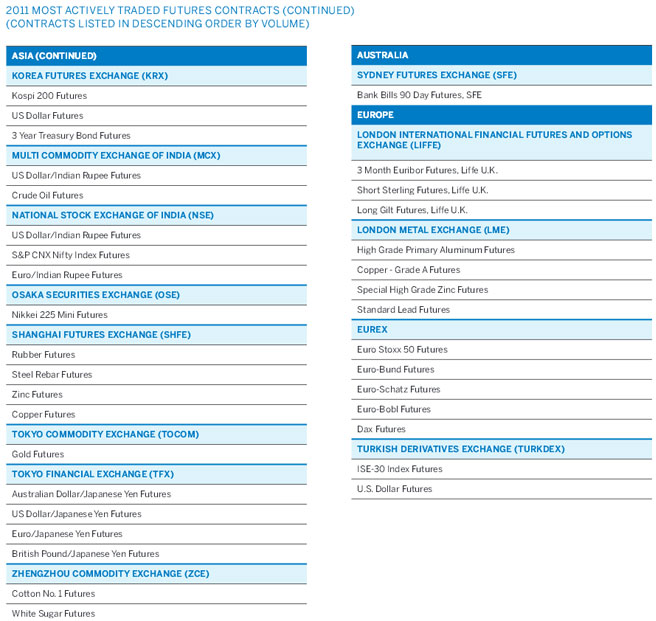

EASE OF GLOBAL DIVERSIFICATION

The substantial growth of futures exchanges across the globe affords trading advisors countless opportunities to diversify their portfolios by geographic markets, as well as by product. Trading advisors thus have ample opportunity for profit potential and risk reduction among a broad array of non-correlated markets. Investing in managed futures on a global scale provides protection against geo-specific variables such as poor weather or political unrest, which could affect some commodities or financial futures more than others.

4. OPPORTUNITY TO PROFIT IN A VARIETY OF ECONOMIC ENVIRONMENTS

Managed futures trading advisors can generate profit in both increasing or decreasing markets due to their ability to go long (buy) futures positions in anticipation of rising markets or go short (sell) futures positions in anticipation of falling markets. Moreover, trading advisors are able to go long or short with equal ease. This ability, coupled with their limited correlation with most traditional asset classes, have resulted in managed futures funds historically performing well relative to traditional asset classes during adverse conditions for stocks and bonds.

For example, during periods of hyperinflation, hard commodities such as gold, silver, oil, grains and livestock tend to do well, as do the major world currencies. Conversely, during deflationary times, futures provide an opportunity to profit by selling into a declining market with the expectation of buying, or closing out the position, at a lower price. Trading advisors can even use strategies employing options on futures contracts that allow for profit potential in flat or neutral markets. This ability to accommodate and protect against unpredictable events can be invaluable in today’s volatile global markets.

5. LIMITED LOSSES DUE TO A COMBINATION OF FLEXIBILITY AND DISCIPLINE

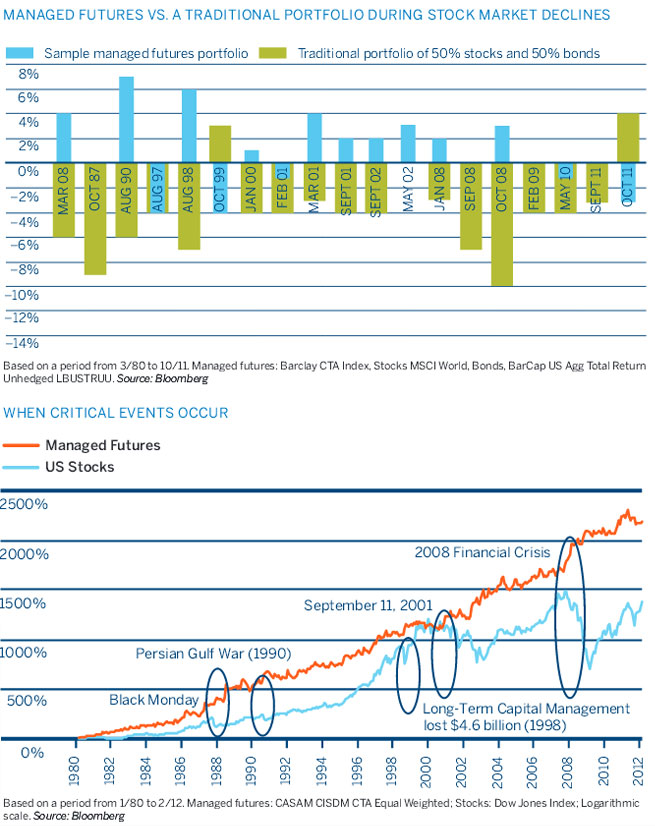

POTENTIAL TO LIMIT DRAWDOWNS

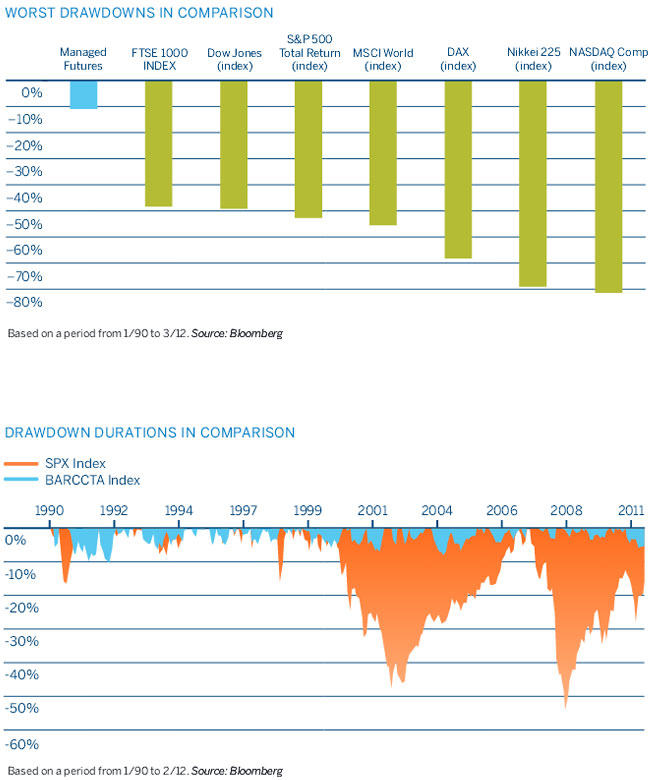

Drawdowns, or the reduction a fund might experience during a market retrenchment, are an inevitable part of any investment. However, because managed futures trading advisors can go long or short – and typically adhere to strict stop-loss limits – managed futures funds have historically limited their drawdowns more effectively than many other investments. As the following chart shows, drawdowns for managed futures have been less steep than those for major global equity indices.

ABILITY TO RECOVER QUICKLY

Additionally, managed futures have historically had shorter recovery times from drawdown periods. This is due in part to the ability to use short trading to take advantage of falling markets, as well as the fact that managed futures often have smaller losses to recover.

With reference to the previous chart, the maximum drawdown for stocks was -52.6% in 2009 whereas the maximum drawdown for managed futures was -10.1% in 1992. It takes much longer to make up for such large drawdowns. To simply recover, the stock index needed to increase by 80 percent from the new low levels.

THE EFFICIENCIES PERFORMANCE AND OF FUTURES MARKETS

While managed futures are new to some, banks, corporations and mutual fund managers have used the underlying futures markets to manage their exposure to price change for decades. Futures markets make it possible for these companies “to hedge” or transfer their risk to other market participants, including speculators, who assume this risk in anticipation of making a profit.

Without speculators, price discovery would only occur when both a producer and an end user want to execute a transaction at the same time. When speculators enter the marketplace, the number of ready buyers and sellers increases and hedgers are able to execute larger orders at their convenience generally without effecting a dramatic change in price – providing additional liquidity, which helps ensure market integrity. By selling futures when prices are rising and purchasing as prices fall, their activity can have a stabilizing effect in volatile markets.

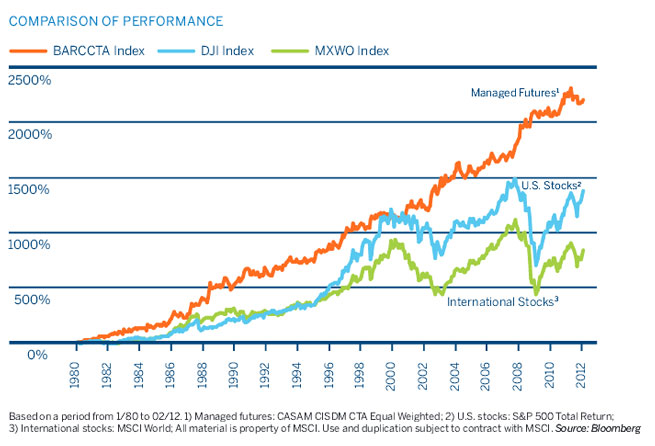

While past performance is not a guarantee of future performance, looking back over the past few decades, managed futures have consistently outperformed asset classes such as stocks and bonds. Consider a hypothetical example with an initial investment of $10,000 invested in 1980. If placed in a U.S. stock fund mirroring the DJI Index, the investment would have been worth approximately $140,618 as of early 2012.

Allocating the same amount to a basket of international equities reflecting the Morgan Stanley Capital International Index of world stocks, the initial investment would have grown to nearly $85,000. But the same investment in managed futures, based on the Barclay CTA Index, would now be worth more than $285,000.

MANAGED FUTURES TRADING STRATEGIES

Fund managers’ investment strategies tend to fall into one of two primary categories: the major group is known as trend followers, while the other is comprised of market-neutral traders.

Many trend followers use proprietary technical or fundamental trading systems which provide signals of when to go long or short in anticipation of upward or downward market moves (trends). While some trend followers employ discretionary systems based on fundamental data and the discretion of the fund manager, the majority use fully automated technical trading systems based on a highly objective, disciplined set of rules predefined by the fund management. By removing human emotion, such as fear and greed, from trading decisions, fully automated trading systems rely on predetermined stop-loss orders to limit losses and let profits run.

Market-neutral traders tend to seek profit from spreading between different financial and commodity markets (or different futures contracts in the same market). Also in the market-neutral category are option-premium sellers who use delta-neutral programs. Both spreaders and premium sellers aim to profit from non-directional trading strategies.

TYPES OF INVESTMENT OPPORTUNITIES

A) Retail or public pools

The recent introduction of low minimum-investment levels for retail funds or public pools provides a way for small investors to participate in an investment vehicle formerly exclusive to large investors. In the United States, fund managers’ business conduct and trading activities are supervised by the Commodity Futures Trading Commission (CFTC) and the National Futures Association (NFA). In addition, offerings of managed futures funds to the general public are regulated by the CFTC, NFA, the Securities and Exchange Commission (SEC), the Financial Industry Regulatory Authority (FINRA) and individual state regulatory agencies. Public managed futures funds must be audited by independent account firms and follow strict disclosure requirements.

B) Individual accounts

Individual accounts are customized accounts for institutional investors or high net-worth individuals. These funds usually require a substantial capital investment so the advisors can diversify trading among a variety of market positions according to the investors’ specifications. For example, certain markets may be emphasized or excluded. Contract terms may include specific termination language and financial management requirements.

C) Private pools

Private pools combine money from several investors and usually take the form of a limited partnership. Most of these pools have minimum investments that can be as high as $250,000. These accounts usually allow for admission and redemption on a monthly or quarterly basis. The main advantage of private pools is the economy of scale that can be achieved for mid-sized investors.

Each of these alternatives may be structured with multiple trading advisors with different trading approaches, providing the investor with maximum diversification.

PARTICIPANTS IN THE MANAGED FUTURES INDUSTRY

There are several types of industry participants qualified to assist interested investors. Keep in mind that any of these participants may, and often do, act in more than one capacity. Please also note that both CTAs and CPOs are registered with the NFA and CFTC.

Commodity Trading Advisors (CTAs) are responsible for the actual trading of managed accounts. There are approximately 1,800 CTAs registered with the NFA, which is the self-regulatory organization for futures and options markets. The two major types of advisors are technical traders and fundamental traders. Technical traders may use computer software programs to follow pricing trends and perform quantitative analyses. Fundamental traders forecast prices by analysis of supply and demand factors and other market information. Either trading style can be successful and many advisors incorporate elements of both approaches.

Futures Commission Merchants (FCMs) are the brokerage firms that execute, clear and carry CTA-directed trades on the various exchanges. Many of these firms also act as commodity pool operators and trading managers, providing administrative reports on investment performance. Additionally, they may offer customers managed futures funds to help diversify their portfolios.

Commodity Pool Operators (CPOs) assemble public funds or private pools. In the United States, these are usually in the form of limited partnerships. There are approximately 1,100 CPOs registered with the NFA. Most CPOs hire independent CTAs to make trading decisions. CPOs may distribute their funds directly or act as wholesalers to the broker-dealer community.

Investment Consultants can be a valuable resource for institutional investors interested in learning about managed futures alternatives and in helping implement a managed fund program. They can assist in selecting the type of fund program and management team that would be best suited for the specific needs of the institution. Some consultants also monitor day-to-day trading operations (e.g., margins and daily mark-to-market positions) on behalf of their institutional clients.

Trading Managers are available to assist institutional investors in selecting CTAs. These managers have developed sophisticated methods of analyzing CTA performance records so they can recommend and structure a portfolio of trading advisors whose historic performance records have a low correlation with each other. These trading managers may develop and market their own proprietary products or they may administer funds raised by other entities, such as brokerage firms.

EVALUATING RISK FROM AN INVESTOR’S PERSPECTIVE

As with any investment, there are risks associated with trading futures and options on futures. The CFTC requires that prospective customers be provided with risk-disclosure statements. Investors that wish to place funds with a CTA or in managed futures should thoroughly review any and all documents including risk documents, disclosure documents, prospectuses, annual reports, etc. before making an investment. Past performance is not necessarily an indicator of future results.

When choosing a managed futures fund, it is important to ensure the fund manager has a proven track record. Before investing, it is also advisable to check the magnitude and duration of the fund’s worst drawdown, or cumulative loss in value from any peak in performance to the subsequent low. In addition, there are several indices that measure managed futures performance. Investors may wish to consult each index to determine which provides the most appropriate performance criteria for their needs. At right is a list of some of the more familiar indexes.

Managed Futures Indexes (Actively Managed):

- Barclay CTA Index

- MLM (Mount Lucas Management) Index

- CISDM Managed Futures Benchmark Series

HOW FEES ARE STRUCTURED FOR MANAGED FUTURES

Total management fees in the managed futures industry tend to be higher than those in the equity markets. While management fees do vary according to the type of managed futures account and may be negotiable, a general fee structure exists. Investors should fully understand that performance information for a managed futures account or fund is almost always expressed net of all such fees.

Typically, the trading advisor or trading manager is compensated by receiving a flat management fee based on assets under management, in addition to a performance “incentive” fee based on profits in the account. The performance fee is almost always calculated net of all costs to the account, such as management fees and commissions. The performance fee is thus based on net trading profits, which are usually paid only if the account or fund exceeds previously established net asset values.

A few trading managers assume the “netting risk,” whereby the performance results of all trading advisors in the account are netted before the investor is charged a performance fee. The trading manager assumes the netting risk by paying each CTA according to his or her individual performance.

In addition to management and performance fees, an account or fund pays transaction costs or brokerage commissions. These expenses reflect the cost of executing and clearing futures trades and generally are calculated on a per-round-turn basis.

INVESTOR SAFETY IS PARAMOUNT IN THE FUTURES MARKET

Protecting the interests of all participants in the futures market is the responsibility of exchange and industry members as well as federal regulators. Working together, they ensure the financial and market integrity required by investors. A brief overview of CME Clearing will illustrate why the credit risk of exchange-traded products is minimal for futures investors.

The market integrity of CME Group …

Rules of the CME Group exchanges are designed to support competitive, efficient and liquid markets. These rules and regulations are reviewed continuously and are periodically amended to reflect the needs of market users. Making sure that trading practices and regulations are followed is the responsibility of the exchange’s Market Regulation and Audit Departments, which work to prevent trading irregularities and investigate possible violations of exchange and industry regulations. The departments provide daily on-site surveillance of trading activity, continuous monitoring of member firms’ trading practices with state-of-the-art technology and prompt, thorough investigations of any customer complaints.

… Combined with the financial integrity of CME Clearing

Clearing operations are another mechanism used by exchanges to uphold the integrity of the futures markets. CME Clearing 1) acts as a guarantor to clearing member firms for trades it maintains; 2) reconciles all clearing member firm accounts each day to ensure that all gains have been credited and all losses have been collected; and 3) sets and adjusts clearing member firm margins for changing market conditions.

CME Clearing settles the account of each clearing member firm at the end of the trading day, balancing quantities of contracts bought with those sold. In clearing trades, the clearinghouse substitutes itself as the opposite party in each transaction, essentially eliminating counterparty credit risk. It interposes itself as the buyer to every seller and the seller to every buyer and becomes, in effect, a party to every clearing member transaction. Because of this substitution, it is no longer necessary for a buyer (or seller) to find the original seller (or buyer) when offsetting a position. A market participant merely executes an equal and opposite transaction, usually with an entirely different party, and ends up with a net zero position.

One of the most important financial safeguards in ensuring performance on futures contracts is the performance bond, which is a deposit clearing member firms must post and maintain against their open positions. These performance bonds, also referred to as margins, are set by CME Clearing based on each product. Your broker may require a larger deposit for your account than CME Group requires of its clearing members.

CME Clearing settles its accounts daily. As closing or settlement prices change the value of outstanding futures positions, the clearinghouse collects from those who have lost money as a result of price changes and credits those funds immediately to the accounts of those who have gained. Thus, before each trading day begins, all of the previous day’s losses have been collected and all gains have been paid or credited. In this way, CME Clearing maintains very tight control over performance bonds as prices fluctuate, ensuring that sufficient money is on deposit at all times.

Related Posts

Race to Nowhere: Markets Pause Before the Next Big Move

Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere. As of mid-February, the S&P 500 is […]

Systematic vs. Discretionary Trading: Which Strategy Is Right for Your Portfolio?

Investors face many choices when selecting investments. Historically, the main divide was between fundamental and technical trading. The growth of computer systems for trading has introduced a potentially larger variable that will only increase as AI advances, whether in systematic (rules-based) or discretionary (human judgment) trading. In just my 20 years working in the industry, […]

The Evolution of Trading from Systematic to AI

Is AI the next step in the evolution of trading? History proves new tools storm the markets, then high adoption erases their edge. What can futures trading history teach us about AI’s trajectory? The 1980s: Rise of Rules-Based Trading Building on simple regression models that aimed to identify patterns across sectors, the 1980s showed that […]