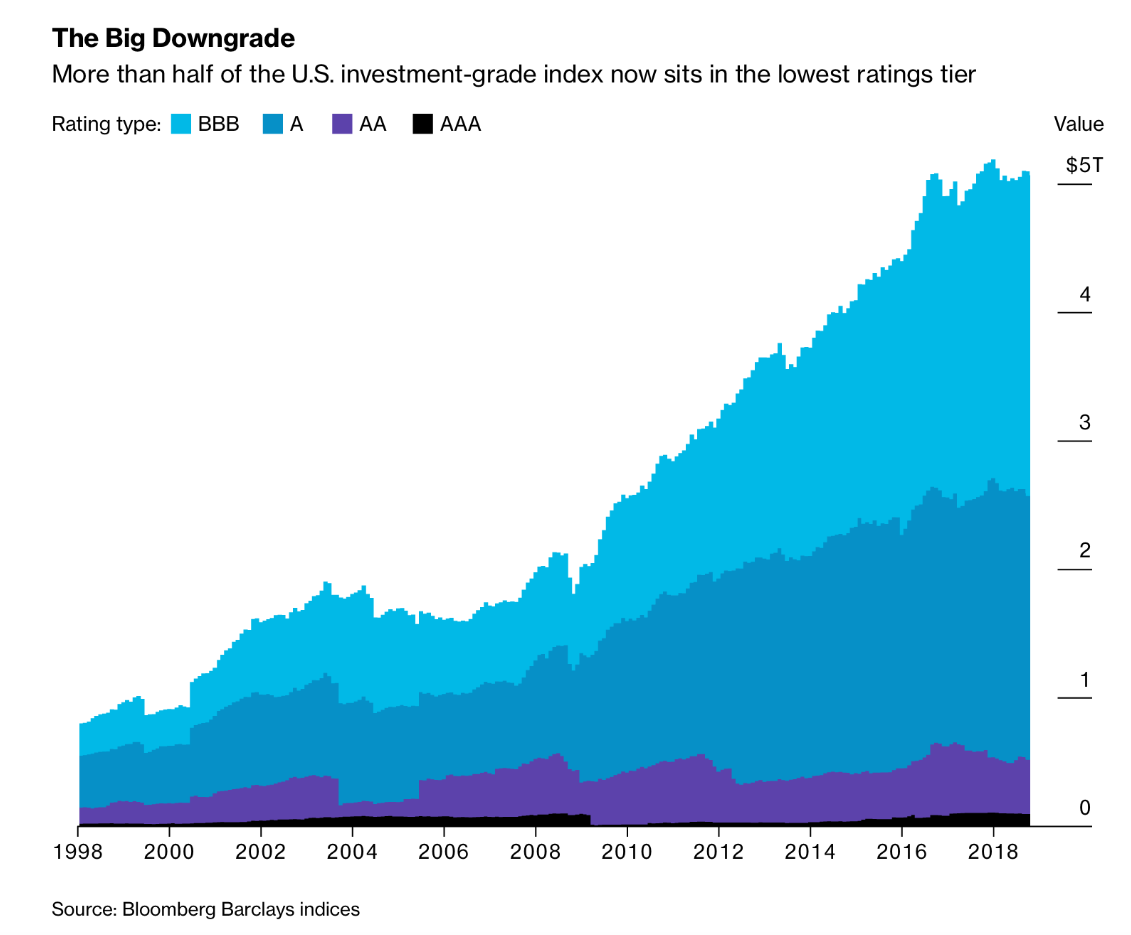

There is no question that the explosion of corporate debt has caught the attention of many investors. This debt growth has been especially strong for BBB-rated companies which on the cusp between investment grade and high yield. Yet, like the boy who cries wolf or the doomsayer who is predicting the end of the world, warnings of a credit crisis do not seem to have affected investor activity. Corporate spreads are still tight and the reach for yield has continued almost unabated. Investors have not been given reasons to care about this debt issue today and have pushed any risks into the future.

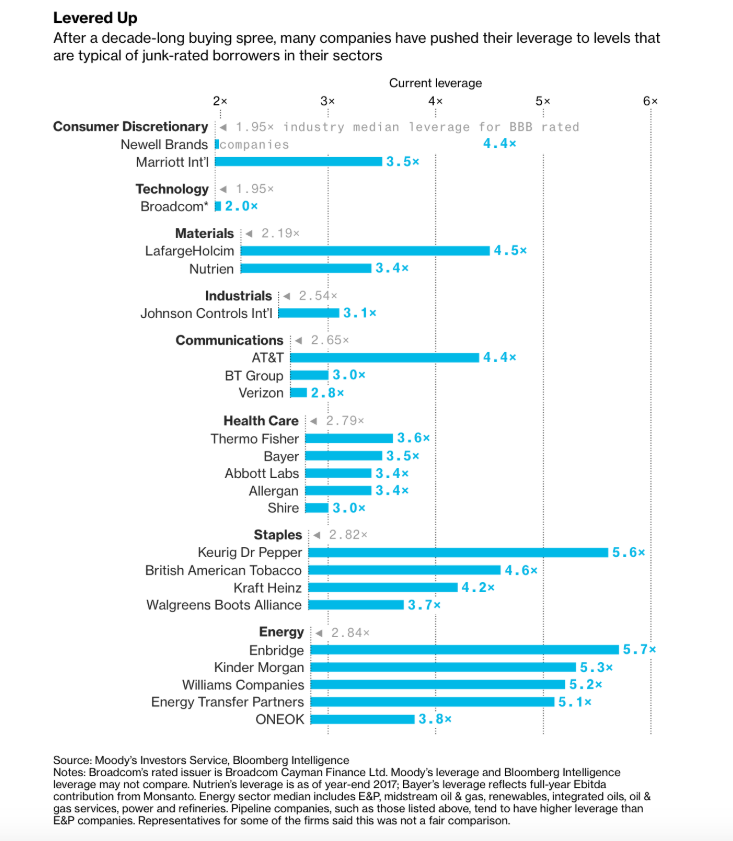

The potential risk for credit is always front and center with any discussions about a new financial crisis but usually the conversation stops there. There is less discussion on what is going on under the hood with respect to credit markets. A recent Bloomberg story highlighted some of the issues that should frighten any investor, see “A $1trillion dollar powder keg threatens the corporate bond market”. This article outlines one scary feature of the added debt; the junk bond leverage for some investment grade firms. This article suggests that rating agencies are not doing their job. We have seen this story before with rating agencies and structured finance. The story implies that when the next macro shock occurs, there are some very large issuers who will see significant declines.

The size of debt may not increase the likelihood of a negative shock. The increase in debt changes the sensitivity to any credit or macro shock. The increased shock sensitivity is what should be feared. A simple walk through of some scenarios shows why investors should be concerned. A lot of this sensitivity spills over to equity markets, which will have a macro wealth effect.

The refinance effect – Much of this corporate debt will have to be refined in an environment that will have higher interest rates; consequently, the cost on firms will increase and push down earnings. Funds will have to be used to delever, or marginal companies may not be finance this new debt. Not a problem today but the earnings sensitivity to rates will increase in the future.

The index cram down effect – With much of the debt being financed by BBB-rated firms, any downgrade will have costs for investors as portfolios will have to be restructured. Spreads will widen on the pushdown of debt that was investment grade but dropped to high yield indices. For some investors who have yield restrictions, there will have to be a sale of the debt, which will have a flow effect.

The optionality (Merton) effect – Given the Merton liability model of the firm and optionality, equity is viewed as a call option on the value of the firm and debt is a short put option. An increase in leverage makes debt more sensitive to any increase in equity volatility. An equity shock will impact debt holders.

The leveraged equity effect – Leverage will increase the riskiness of the firm, which will impact stocks if there is any macro shock given the costs of restructuring and bankruptcy. Marginal lending will not be available to these firms.

The covenant effect – The demand for debt allowed a reduction in covenant protections. The impact of covenant-lite bonds is straightforward. The covenants add warnings, early protections, and restrictions that all help bondholders. If these are gone, risk increases. While some empirical work suggests that there is no effect from fewer covenants. The testing has not been under stress scenarios. Regulators have asked banks to restrict covenant-lite lending, but the practice continues.

The shadow banking effect – The demand for credit has outstripped the supply available from banks, so hedge funds and private equity have moved into the lending space. The impact of these new players is unknown. My banking experience has always told me that one bank loan chews up the time and resources associated with underwriting many good loans.

The overall effect of more leverage is that the next time there is a macro shock both equity and debt will be more sensitive to a downturn. Investors may not feel any impact today, but when it comes the effect on markets will demonstrable.