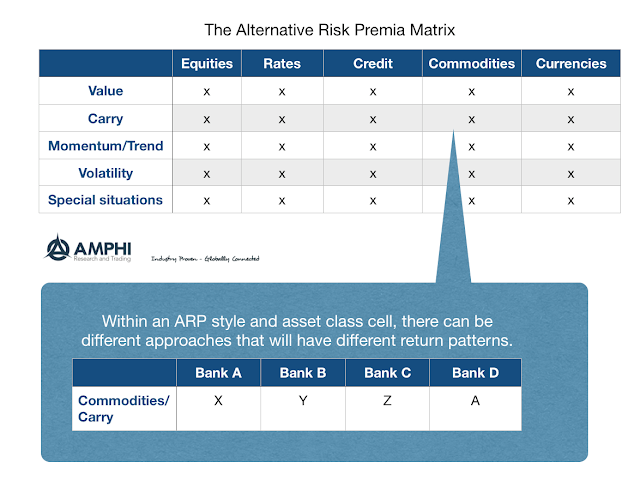

An alternative risk premium (ARP) matrix is an effective way to start any portfolio construction exercise. A matrix divides risk premia through two criteria, asset class and style. We think in terms of a 5×5 style/asset class matrix. The asset classes include: equities, rates, credit, commodities and currencies. These asset classes have inherent differences that make them unique even when looking through an alternative risk premia lens. For alternative risk premia we include: value, carry, momentum/trend, volatility, and special situations. These styles are been well-defined and identify risk premia that can be exploited through forming long/short portfolios and are actively traded and structured through the bank swap market.

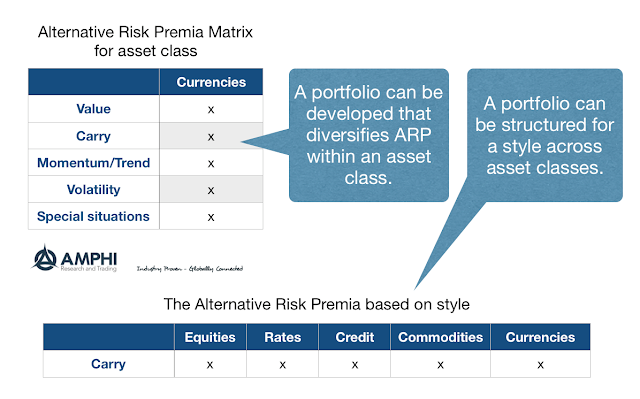

The matrix can create a broadly diversified portfolio across style risk premia found for each asset class. Full diversification would include a range of styles across a broad set of asset classes. An allocation can be made to each of 25 buckets in a 5×5 construct. However, an asset class specific portfolio would diversify across styles and a style specific portfolio will invest that style across all asset classes.

Investors can think in terms of specific asset classes or styles to form different portfolio combinations. For example, in the currency asset class, there are well-defined risk premia that include: value as defined through purchasing power parity; carry through long/short portfolios based on interest differentials; momentum and trend premia based on past price action; volatility premia based on option implied versus realized volatility; and special situations associated with curve plays and liquidity.

A similar matrix exercise can diversify a given risk premia style across asset classes. For example, a portfolio focused on momentum and trend could include allocations in each of the five asset classes identified.

Correlation or cluster analysis can be used to find risk premia, which are uncorrelated, in order to form a diversified portfolio but a risk premia matrix can serve as theoretical basis for portfolio construction. This approach is especially helpful as the set of risk premia expands.

Nevertheless, the risk premia for specific styles and asset class across a number of bank swap providers may not be all the same. Banks which offer risk premia through swaps may create different portfolios to represent a given risk premia. Within a given style and asset class, there can be a cluster of banks that offer different risk premia products. Some may be closely correlated while other can be very different. For example, one bank may not define the alternative risk premia for rates carry the same way as another bank. Additionally, the markets included in the swap index for a given style/asset class combination may differ across bank providers. These swap differences for a specific ARP is a source of competition and differentiation across banks.

The portfolio matrix and structures should account for the differences across ARP products within a styles and asset class bucket. This adds bank specific differences to our portfolio matrix but it does not change the overall story. This framework, albeit simple, provides a useful tool for creating a scaffold for forming a portfolio structure.