Diversification is usually thought of as a longer-term concept. Don’t worry if it seems like you are not receiving diversification in a given month or quarter. Think about diversification across a longer horizon. Diversification also does not guarantee better returns for a portfolio. Negative diversification does mean that your losers will be offset with winners.

Yet, investors often look for diversification protection over short periods. If stocks are going down this month, they are looking for an offset this month. If stocks have had a bad quarter, investors are looking for something good this quarter. That is wishful thinking. Correlations change and the measure is about co-movement relative to mean values.

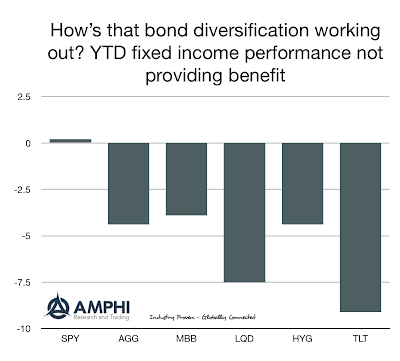

This year has not been good for diversifying assets like fixed income. Our simple chart shows returns for equities and some of the leading fixed income alternatives: the Barclay Aggregate, mortgages, long duration Treasuries, investment grade credit, and high yield. None have worked well at portfolio protection even though fixed income volatility with the exception of long duration Treasuries is less than half of equities. Investors are taking on a high degree of credit and rate risk during Fed tightening late in the business cycle.

An alternative form of diversification is to breakout of asset class risk and switch to style risk that is focused on alternative risk premia. The concept of alternative risk premia is to isolate the risk within an asset class to some constituent components like value, carry, or momentum. This diversifies risk on another level beyond asset class or beta exposure. When blended across a number of premia, this diversification can be done with or without making a focused class decision.

Related Posts

Race to Nowhere: Markets Pause Before the Next Big Move

Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere. As of mid-February, the S&P 500 is […]

Systematic vs. Discretionary Trading: Which Strategy Is Right for Your Portfolio?

Investors face many choices when selecting investments. Historically, the main divide was between fundamental and technical trading. The growth of computer systems for trading has introduced a potentially larger variable that will only increase as AI advances, whether in systematic (rules-based) or discretionary (human judgment) trading. In just my 20 years working in the industry, […]

The Evolution of Trading from Systematic to AI

Is AI the next step in the evolution of trading? History proves new tools storm the markets, then high adoption erases their edge. What can futures trading history teach us about AI’s trajectory? The 1980s: Rise of Rules-Based Trading Building on simple regression models that aimed to identify patterns across sectors, the 1980s showed that […]