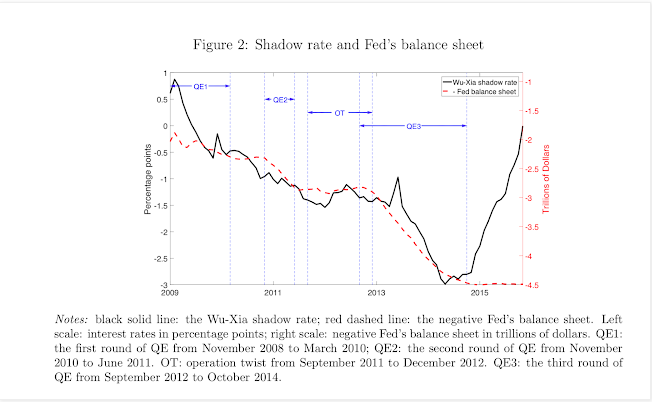

We cannot forget that the zero bound on interest rates caused distortions in market price signals. Now in the US rates are above the zero bound so it seems like the concept of a shadow rate is not important; however, it is still relevant for many other central banks and it provides a good measure of where we have come over the last few years. Using the shadow rate as a historic measure of relative tightening, we can say that the Fed has actually been on a tightening policy since the end of quantitative easing. The size of this tightening is not much different than what we have seen in other Fed tightening cycles. While we cannot measure the true bite of rising rates, we can say that the Fed has been at tightening for much longer than most investors think.

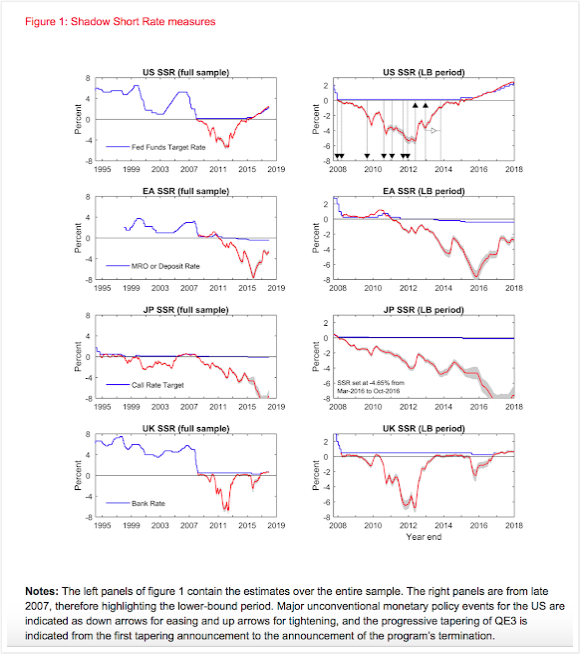

The concept of the shadow interest rate was developed to determine what should be the short-term interest rate when constrained by the zero bound. The shadow rate can be an important tool to look at monetary policy even when rates go above the zero bound because it can give investors insight on where we have been versus where we are with rates.

We use the Central Bank of New Zealand website as a place to check on the shadow short rates around the world.

For example, you cannot think about US rates rising from zero as the amount of tightening seen by the market. Rather investor should think about the rate rise from the minimum of the shadow rate. In this case, the Fed has been tightening for longer and the amount of tightening is significantly more than 200 plus bps. Similarly, there has been a significant rise in the shadow rate associated with the ECB.

Looking at some of the research by the original author on shadow rates, Jing Wu from the University of Chicago, “A Shadow Rate New Keynesian Model”, it is clear that tightening really began when QE ended. The connection with rates is a link that has been missing with many market watchers.

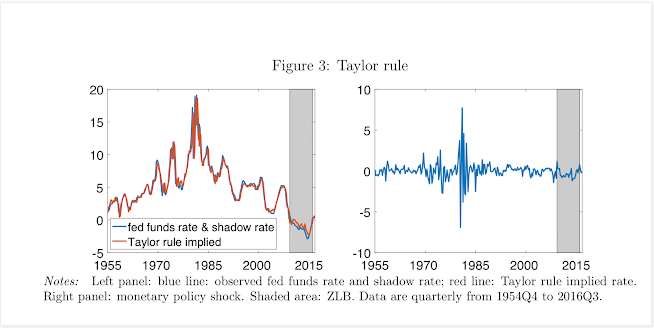

There is a fair amount of estimation error with these shadow rates. It is not precise tool, but we can go back to the Taylor Rule and see that it does a good job of predicting the fed funds rate as well as the shadow rate. The shadow rate is similar to the Taylor Rule implied rate. Track the shadow rate and follow the Taylor Rule and you have a pretty good combination of indicators of what central banks may be up to without relying on reading central bank tea leaves through policy speak.

Related Posts

Race to Nowhere: Markets Pause Before the Next Big Move

Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere. As of mid-February, the S&P 500 is […]

Systematic vs. Discretionary Trading: Which Strategy Is Right for Your Portfolio?

Investors face many choices when selecting investments. Historically, the main divide was between fundamental and technical trading. The growth of computer systems for trading has introduced a potentially larger variable that will only increase as AI advances, whether in systematic (rules-based) or discretionary (human judgment) trading. In just my 20 years working in the industry, […]

The Evolution of Trading from Systematic to AI

Is AI the next step in the evolution of trading? History proves new tools storm the markets, then high adoption erases their edge. What can futures trading history teach us about AI’s trajectory? The 1980s: Rise of Rules-Based Trading Building on simple regression models that aimed to identify patterns across sectors, the 1980s showed that […]