Reviewing the first quarter financial performance, the dominant macro theme was the change in Fed policy actions. The same could be said about the EU—no rate increase and no solid trend for normalization. The new macro focus is on the choice of Fed governors.

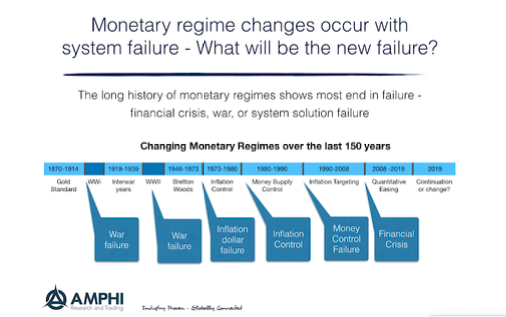

More important than any policy comments or change in Fed governors are the long-run changes in monetary regimes. These regimes are extended periods of dominant policy choices. The regime themes drive the behavior of financial assets. Quantitative easing has been the dominant theme for the last decade, and attempts to reverse this theme have hit a wall.

These themes drive central bank choices only to be discarded when they prove unable to address current problems or the world is punctuated by geopolitical upheaval. Wars cause monetary regime changes. Financial crises require changes as old policies are found to be inadequate. Central bankers only change their dominant policy when change is forced upon them. Failure and disruption are necessary for change. Without a liquidity crisis, don’t expect a new regime. We muddle forward.

Related Posts

Systematic vs. Discretionary Trading: Which Strategy Is Right for Your Portfolio?

Investors face many choices when selecting investments. Historically, the main divide was between fundamental and technical trading. The growth of computer systems for trading has introduced a potentially larger variable that will only increase as AI advances, whether in systematic (rules-based) or discretionary (human judgment) trading. In just my 20 years working in the industry, […]

The Evolution of Trading from Systematic to AI

Is AI the next step in the evolution of trading? History proves new tools storm the markets, then high adoption erases their edge. What can futures trading history teach us about AI’s trajectory? The 1980s: Rise of Rules-Based Trading Building on simple regression models that aimed to identify patterns across sectors, the 1980s showed that […]

From Revolution to Triton Bay: How Mark Chapin’s New CTA Rewrites the Futures Playbook

What makes a futures program great? Obvious answers include excellent performance, low drawdowns, a high Sharpe ratio, or consistent returns. While everyone searches for those qualities, large money managers know that the secret to producing all of those is to build portfolios that target those goals using multiple strategies. After all, high returns and low […]