If I invested based on political rhetoric and news, I would be moving to a safe asset and expect stocks to decline. The uncertainty concerning policy and the animus between political parties and countries would suggest an environment that would not be suitable for the long-term optimism that is needed to see equities march higher. If I read just the financial papers and economic data, I would paint a more optimistic picture with consumer and business surveys both showing a positive environment. If I were a focused policy wonk, I would have a mixed view on market prices with the potential for stimulative policies but still a policy environment where details and specifics are scarce. It is hard to see these differences continuing. As politics, economics, and policy come into focus, there will be a strong reaction in price. Unfortunately, predicting when this alignment will occur is very difficult.

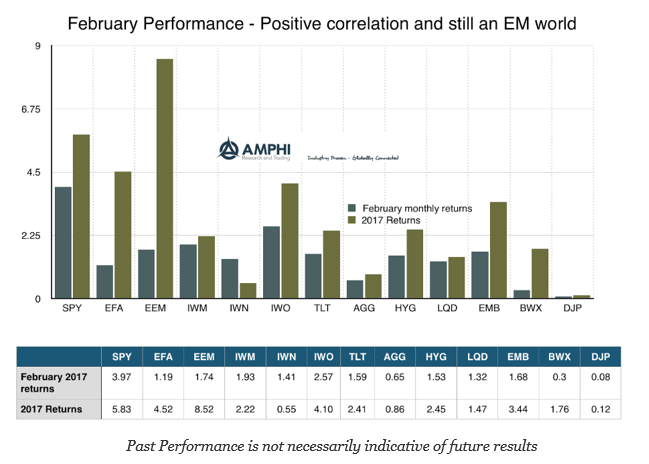

We are surprised with the positive performance across the broad set of asset classes and styles followed monthly. Risky EM stocks and bonds both performed well in spite of the clearer rate rising environment signaled by the Fed. Large cap equities outperformed riskier small cap, value and growth. Long bonds outperformed credit sensitive fixed income. The only asset class without strong movement has been the commodity space. Commodities have seen lower correlation intra-class as these diverse markets have moved away from the negative commodity cycle.