The choice between active and passive investing has been a battle that has been raging for years, but it can be simplified through a set of easy questions. The answers to these questions are not easy, but by forming a direct set of straightforward questions with a decision tree, the issues can be discussed in the open. The first question is about market structure and efficiency.

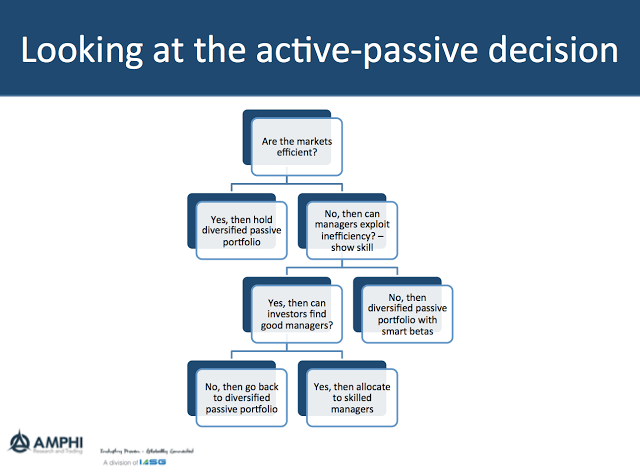

1. Are markets efficient?

If the answer is yes, markets are efficient, then the choice is simple. Invest with passive indices and hold a diversified portfolio. There can be a wide range of answers to the question of what is an appropriate portfolio, but the question of choosing active managers should be off the table. Surprisingly, the market has moved more to passive investing simultaneously as more agree that markets are inefficient. The investor must shift to a second question if the answer is no.

2. Are there managers who can exploit market inefficiencies? That is, are there managers with skill?

Markets can be inefficient, but that does not mean all active managers trying to exploit these inefficiencies have skill. There can still be only a tiny number who have the skill of being able to exploit inefficiencies. If the answer to the question is no, then there could be room for specific strategy benchmarks or smart beta alternatives that may be able to exploit some inefficiencies. For example, strategies could include a rules-based portfolio exploiting inefficiencies through low-cost benchmarking.

3. Can investors identify skilled managers or forecast their performance?

This is not easy because differentiating between managers with and without skill may take a lot of data, and there may be switching between skilled managers based on the environment or successful strategies. For example, a manager could be experienced at value investing but unable to make significant gains when value is out of favor. If an investor cannot identify the manager with skill, he should return to the passive, diversified portfolio.

The conclusion is that any holding of active managers has to be based on the market environment, managers’ quality, and investors’ ability to identify an inefficient environment and skilled managers. Since the markets are generally efficient, good managers are rare, and it is hard to find those managers, active management should be an exception, not the norm.

Related Posts

Race to Nowhere: Markets Pause Before the Next Big Move

Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere. As of mid-February, the S&P 500 is […]

Systematic vs. Discretionary Trading: Which Strategy Is Right for Your Portfolio?

Investors face many choices when selecting investments. Historically, the main divide was between fundamental and technical trading. The growth of computer systems for trading has introduced a potentially larger variable that will only increase as AI advances, whether in systematic (rules-based) or discretionary (human judgment) trading. In just my 20 years working in the industry, […]

The Evolution of Trading from Systematic to AI

Is AI the next step in the evolution of trading? History proves new tools storm the markets, then high adoption erases their edge. What can futures trading history teach us about AI’s trajectory? The 1980s: Rise of Rules-Based Trading Building on simple regression models that aimed to identify patterns across sectors, the 1980s showed that […]