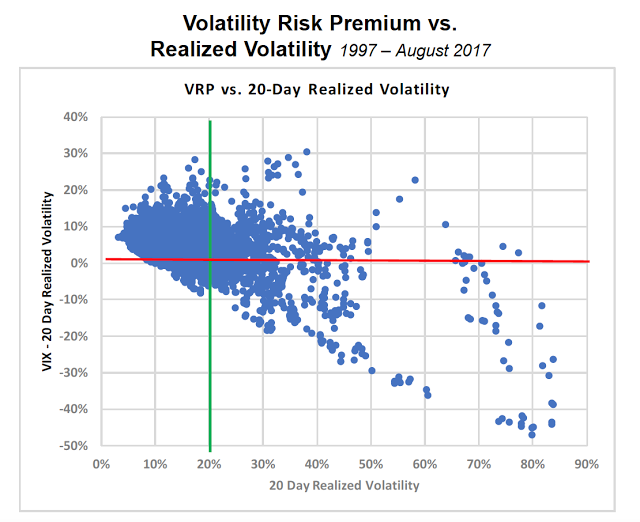

Implied volatility is usually higher than realized volatility so there is a positive volatility risk premium, except when there is a crisis or volatility spike at which time the volatility premium turns negative. A recent CBOE seminar presented a chart on the volatility premium to illustrate the risk.

The numbers suggest that being short volatility gave you a positive premium in a stable world, but when the world is less stable, (higher realized volatility), you do not want to be a vol seller. The chart suggests that there can still be a positive risk premium when realized volatility is high, but the odds work against you. It is a way to get to a realized volatility of more than 20% at current levels, but that world can become a reality quickly if there is an equity sell-off.

It is important to measure your short volatility where you may have been picking up vol premium. If you have too much, now is the time to cut that exposure.

Related Posts

Anatomy of a Tough Month for Trend-Followers: Tariff Shocks & Volatility Spikes

It is often said that trend followers provide “crisis alpha.” This means that market stress often benefits their strategies. This follows logically as moves get larger, coordinate together, and run consistently, trading becomes easier. These managers quickly caution that they do not always provide this negative correlation. Price action can swing unpredictably against long-standing trends […]

Time-varying correlation – Diversification benefits are dynamic

What is the correlation between two assets? The correlation is critical because it is the driver for any diversification decision. The better question is, “What is the correlation now, and what can it be in the future?”. Correlations are often time varying and regime specific. In bad times, correlations rise, so the diversification expected is not present when you need it. This phenomenon requires more thinking about tail risks and how to best address them.

The “3 by 5 Index Card” on What You Need to Know About the February VIX Spike

University of Chicago professor Harold Pollack in an interview a few years ago mentioned that the best money advice can fit on a three-by-five inch index card. He was then challenged to write the card. His financial advice went viral. We follow this tradition by focusing on a simple “three-by-five index card” on the VIX volatility spike earlier the month.