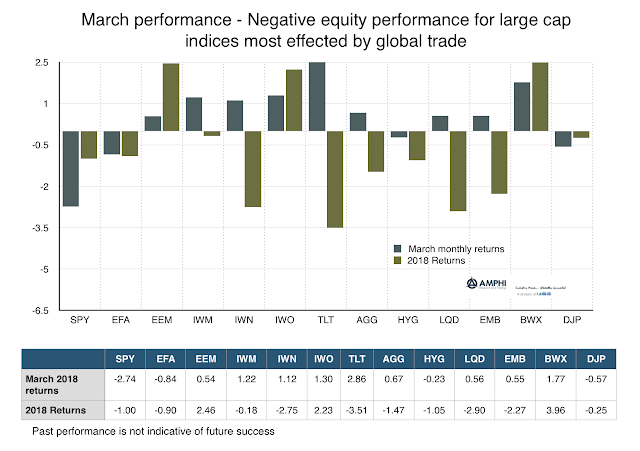

Markets have seen a significant change in economic sentiment over the first quarter of 2018. Market views have moved from euphoria concerning tax cuts and global growth, to the fear of a volatility shock, to a revised view of growth, and finally to growth fears under the concern that a trade war is around the corner. Overall, major assets, both equities and fixed income were negative for the quarter. Large cap firms that engage in global trade were hurt in March while bonds rallied as the safe asset. US small cap equities did better given their focus on domestic growth. Emerging markets gained on the dollar decline and the continued belief that EM markets have room for independent growth.

As we start the second quarter, the economic growth picture looks more mixed and earnings may be under pressure if there is no further growth beyond tax cut adjustment. The continued high volatility with the VIX index, albeit lower than the early February extremes, is averaging between 18-20% and putting further pressure on repricing of risk. With higher short-term interest rates, the value of discounted cash flows has fallen and there is less demand for risky assets. While the growth and liquidity signs are not flashing a strong exit from risky assets, caution is required and any new savings is best positioned in safe assets. The weight of the evidence is signaling portfolio positioning toward low risk or uncorrelated assets. Any risky asset over-weights should be adjusted downwards.