The film noir, “DOA”, had a great premise – a man staggers into a police station and wants to report a murder – his own. He was poisoned and had a limited time to find his killer and why. The hedge fund industry 2/20 fee schedule is dead. Some managers may not know it yet, some are in denial, but it happened and now it is just a matter of sifting through the suspects to find the killer.

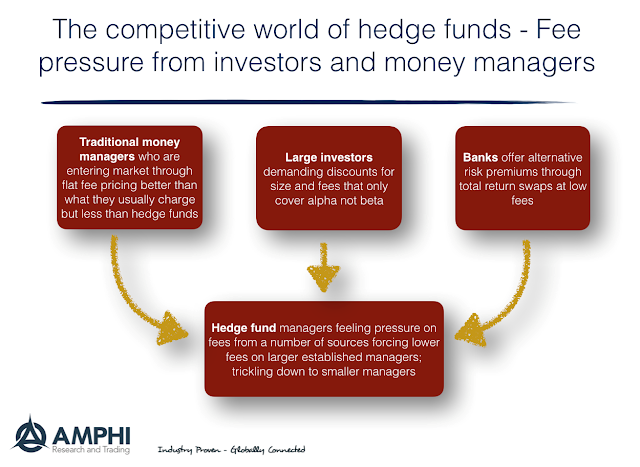

Most observers think customers are the drivers who forced a change in fees. There is no question that large investors have been pushing lower fees on managers, Managers can accept the fee reductions because they have economies of scale, but I will suggest a different premise; the competitive forces outside the hedge fund industry.

The key forces today are not from within the hedge fund universe albeit that is happening, and the forces are not just from investors albeit they have gotten smarter and have demanded more from managers. Banks are the key competitors through their swaps desks which offer alternative risk premium indices.

Since Dodd-Frank, banks have looked for other sources of trading income. Offering swap products is a direct threat to hedge funds that are often generating returns through a combination of alternative risk premiums (ARPs). The banks can offer ARPs at low cost, high liquidity, and full transparency. Pricing can be a simple fee embedded in the swap index. The banks get flow, fees, and customers. Investors face a money center rated bank versus a hedge fund which will be significantly smaller. These “generic” products often match or better the performance of hedge funds and provide better terms.

Hedge funds who are competing for the institutional market have little choice but to lower fees to similar levels offered by bank swaps. A hedge fund does not have to just argue that he is better than the other hedge fund down the street but that he is also better than an ARP index that is being offered by a big money center bank. Institutional investors can play these added competitors against each other to ensure the best price and product. The survival of premium pricing is only through specialized hedge fund skill. Tell me how 2/20 or some variation of management and incentive fee can survive?