Investors should have a growing concern with the reach for yield in the current market. The reach for yield has pushed investors into illiquid issues where the risk profile has changed from credit/carry to credit/carry/illiqudity. Investors will generally receive a higher premium if an asset is illiquid. Unfortunately, illiquidity premiums are hard to measure; consequently, the traditional credit betas will not be properly measured and there could be the mistaken view that there is greater alpha from managers who hold these types of assets.

Holding these investments may become painful if there is a change in the credit cycle and there is a need for liquidity but the market becomes one-sided. There is a difference between being paid for credit risk and being paid for illiquidity. Credit risk will be associated with the underlying risk of the firm while illiquidity premium will be associated with the inability to find buyers when a sale is desired. Illiquidity is the uncertainty with matching buyer and seller and not with the underlying risk of the credit. Illiquidity, given it being situational, is inherently difficult to price.

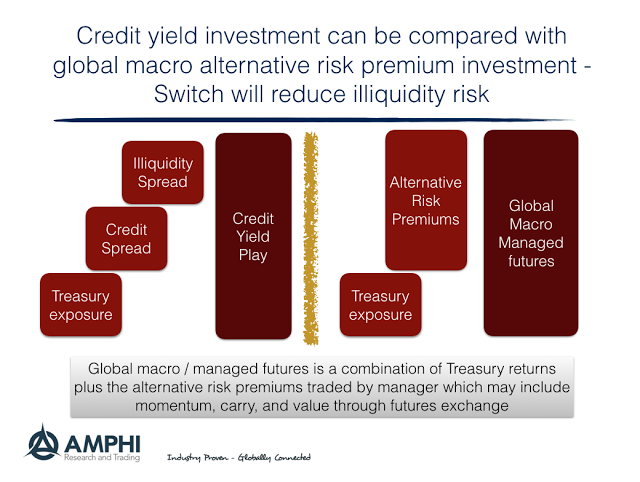

If there is the belief that liquidity and credit are become more expensive, it may be appropriate to switch risk premiums. We suggest that the risk premiums switch from credit to macro through managed futures. Managed futures managers will often blend risk premiums like momentum, carry, and value across major asset classes, but do it through using liquid instruments traded on futures exchanges.

Since the futures investments requires low margin for a given notional value and the reminder of a cash investment can be held in Treasury, the managed futures investment can be compared to a credit investment. Credit and liquidity spreads can be compared against the average excess return for global macro/managed futures. Right now, the return required to beat a credit play is at low levels, so a managed futures investment is attractive and also will solve the potential growing liquidity risk problem.