“…for it is a recognized characteristic of money as a store of wealth that it is barren; whereas practically every other form of storing wealth yields some interest or profit. Why should anyone outside a lunatic asylum wish to use money as a store of wealth? Because, partly on reasonable and partly on instinctive grounds, our desire to hold money as a store of wealth is a barometer of the degree of our distrust of our own calculation and conventions concerning the future.”

-Keynes

“Money is not a store of value but a claim on value. “

– Brett Scott

As rates start to move higher, it is important to go back to basics on what is the value of money and whether it should be used as a store of value. In a zero or negative interest rate environment, holding money is a good rational strategy, but times are changing especially in the US. This is not the case in the EMU where short rates are still negative and holding cash makes sense.

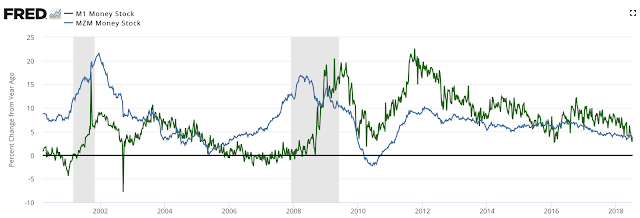

There was a significant search for yield given the absolute level of rates as investment substitutes. That search for yield involved taking more risk. Now there should be a search for alternative stores of value through moving out of currency and demand deposits for near cash. With inflation higher, the cost of money as a store of value increases. The change in money stock will slow given the change in portfolio balances.

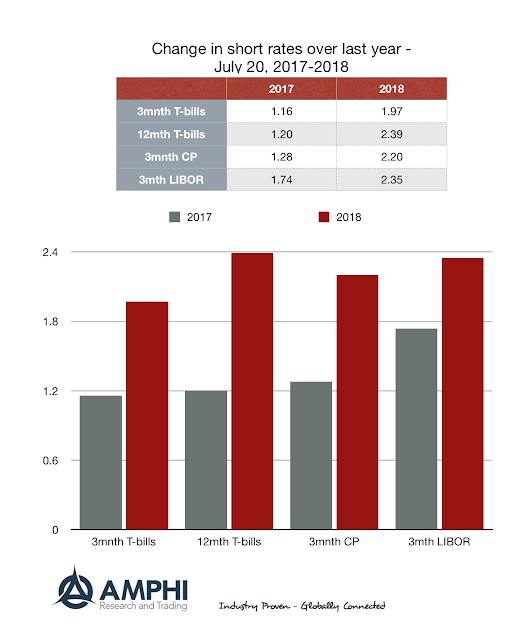

However, care is needed to find the right store of value. Moving too far out the curve in the credit area has been costly given the widening in spread in corporate bonds. Floaters still face spread risk. Short-term Treasuries and agency paper are still a go-to choice for 2 percent yields; nevertheless, there are some short-term corporate paper that offer better yields.

The only reason not to hold these yield instruments is if you have a wildly high aversion to risk or you believe there is so much uncertainty that even 3-month yields cannot be trusted. That is not the case so money should be moved out of cash regardless of any current financial asset uncertainty.