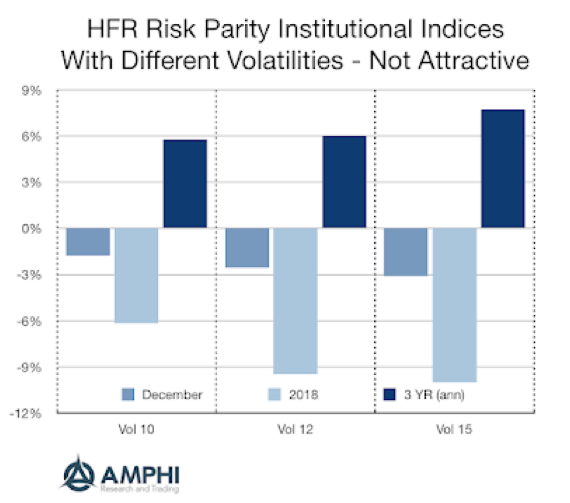

Risk parity was thought of as a portfolio strategy that would protect investors buffeted with uncertainty. Don’t think about dollar allocations, but risk allocations; it is a better way to manage a portfolio. Unfortunately, theory does not always work in practice. Using a simple benchmark of the average return for mutual funds with 50-70% equity allocation would have had slightly better returns than the 10% risk parity index and would have done much better than the higher vol indices in 2018.

When no asset class does well and volatility is targeted at higher levels, risk parity cannot save an investor from loses. A combination of two volatility shocks, February and the fourth quarter, was enough to cause under performance. Levered into a volatility spike and then de-levered on the reversal after the spike will create a whipsaw effect. There is no safe harbor with risk parity. Does this mean investors are done with the strategy? It will still have advocates, but there will be a search for new portfolio solutions.

Set it and leave it alone portfolio management has significant costs when there are regime changes. While active discretionary management may not be a solution, systematic rules that address regime change will help with allowing for some flexibility when there is a market change.