DISCLAIMER:

While an investment in managed futures can help enhance returns and reduce risk, it can also do just the opposite and in fact result in further losses in a portfolio. In addition, studies conducted of managed futures as a whole may not be indicative of the performance of any individual CTA. The results of studies conducted in the past may not be indicative of current time periods. Managed futures indices such as the Barclay CTA Index do not represent the entire universe of all CTAs. Individuals cannot invest in the index itself. Actual rates of return may be significantly different and more volatile than those of the index.

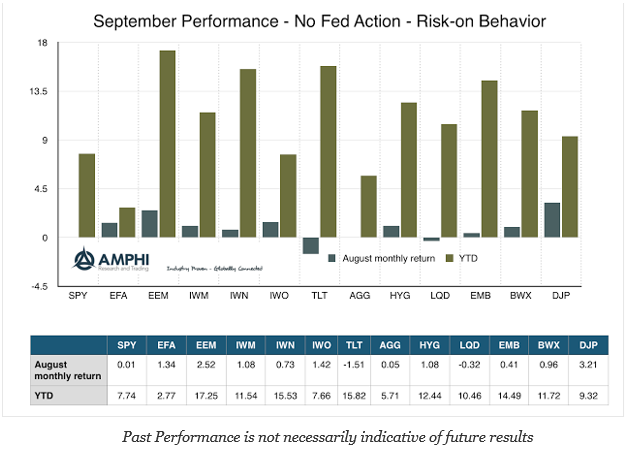

Was investing for the month so simple? The Fed did not take any action, albeit the threat that they are getting close, and the markets rallied for the month. Fade the Fed regardless of their speeches about wanting to move rates higher. We think this strategy may be ending in December, but right now investors were again rewarded for not believing any threats of Fed action.

Granted there were other cross-winds which affected asset performance, but the story was once again central bank behavior. Hold risky assets and sell the uncorrelated safe asset, long bonds. While the S&P 500 was flat for the month, small cap, value, and growth all gained in September. Global equities also gained albeit with an increase of only a little one percent given the more uncertain outlook in Europe and Japan. With no Fed rate increase, emerging markets were the big winner at up over 2.5 percent.

Bonds showed mixed results with long duration bonds falling in value given the Fed comments that the rate rise is close, perhaps in December. High yield gained on higher oil prices and a general willingness to engage risk-taking. We have concerns with the increase in bankruptcies this year, but the markets don’t seem to give this much weight. Non-dollar exposures in both developed and emerging markets gained on lower dollar funding pressure. Commodities gained on the favorable risk environment and gains from the OPEC production cut announcement.

Investors who had concerns about the Fed raising rates multiple times or the risk from slowing economic growth missed seven months of good performance. We have a special concern about the reduced negative correlation between stocks and bonds recently as well as the spiking of volatility over short horizons. Nevertheless, a combination of emerging market equity and long bonds, a weird barbell of risk and protection would have combined for over 15 percent return this year.

What looked like a poor year at the end of the first quarter is shaping up to be very positive as we move into the fourth quarter. An ongoing pessimism about the fundamentals for risky assets has not been rewarded, yet with the US election and the threat of a Fed activity, there may be enough risks to reverse some of the positive performance in the next three months.