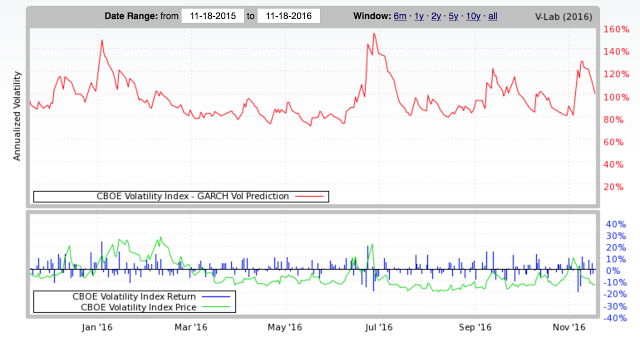

A close look at volatility across major asset classes over the last year shows that the BREXIT vote was a much bigger market event than the US presidential election. Looking at stock, bond, and currency volatility over 2016 suggests that the uncertainty post-election has not been as great as the BREXIT shock and already seems to be reversing.

The stock market volatility jump was much bigger for BREXIT as measured by the VIX. In fact, the early year sell-off also saw a greater spike in volatility. Stock market volatility also seems to be declining faster after the election spike although it is following the normal pattern of spiking and then declining slowly through time.

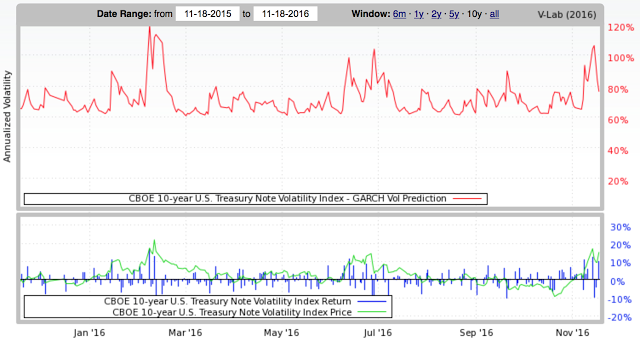

The bond volatility spike was much greater during the realignment of risks after the first of the year. The equity sell-off in the first two months of 2106 was coupled with a significant switch into bonds. For bonds, the BREXIT and election spikes were similar although bonds showed an extended period of volatility in the late second quarter. The BREXIT and Fed uncertainty coupled for a longer period of volatility during June.

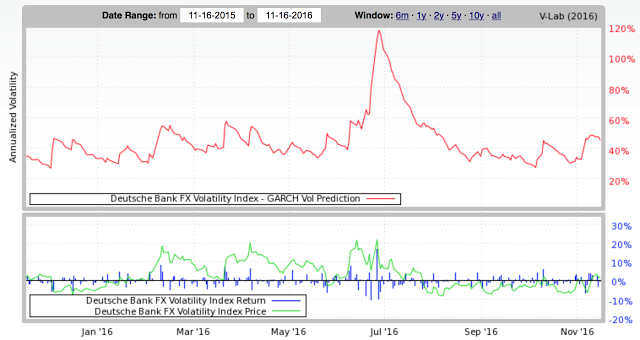

Currency market volatility increased upon the election results but was not notably different than increases associated with some central bank announcements this year. For currencies, BREXIT was a much bigger deal by an order of magnitude of three.

We use volatility as a sign of heterogeneous expectations. If there is less clarity on the direction of markets and it is harder to discount market information, there will be a spike in volatility regardless of market direction. There was a shock effect with the election, but there seems to be a normalization of views concerning the new president. This does not mean there will not be market directional trends based on policy expectations. Directional trends and volatility are different. Volatility may spike again but not until we have some new policy news to discount.

Related Posts

Anatomy of a Tough Month for Trend-Followers: Tariff Shocks & Volatility Spikes

It is often said that trend followers provide “crisis alpha.” This means that market stress often benefits their strategies. This follows logically as moves get larger, coordinate together, and run consistently, trading becomes easier. These managers quickly caution that they do not always provide this negative correlation. Price action can swing unpredictably against long-standing trends […]

Time-varying correlation – Diversification benefits are dynamic

What is the correlation between two assets? The correlation is critical because it is the driver for any diversification decision. The better question is, “What is the correlation now, and what can it be in the future?”. Correlations are often time varying and regime specific. In bad times, correlations rise, so the diversification expected is not present when you need it. This phenomenon requires more thinking about tail risks and how to best address them.

The “3 by 5 Index Card” on What You Need to Know About the February VIX Spike

University of Chicago professor Harold Pollack in an interview a few years ago mentioned that the best money advice can fit on a three-by-five inch index card. He was then challenged to write the card. His financial advice went viral. We follow this tradition by focusing on a simple “three-by-five index card” on the VIX volatility spike earlier the month.