DISCLAIMER:

While an investment in managed futures can help enhance returns and reduce risk, it can also do just the opposite and in fact result in further losses in a portfolio. In addition, studies conducted of managed futures as a whole may not be indicative of the performance of any individual CTA. The results of studies conducted in the past may not be indicative of current time periods. Managed futures indices such as the Barclay CTA Index do not represent the entire universe of all CTAs. Individuals cannot invest in the index itself. Actual rates of return may be significantly different and more volatile than those of the index.

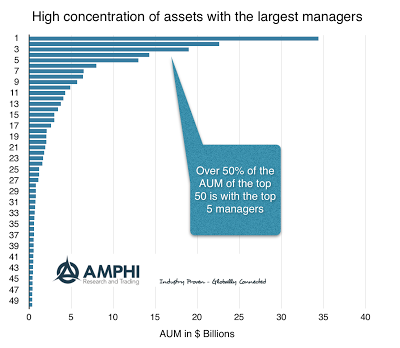

CTA Intelligence reported the top 50 CTA’s as of September 2016 and provided some good graphics on the names and the changes over the last year. Taking a closer look at the data from the perspective of market structure and industrial organization provides some additional insights on the managed futures industry. We will focus the discussion on the top 50 managers because these are the ones that will receive the most interest from institutional investors. We can call this the relevant market.

The market share of the top 5 managers is highly concentrated with those managers having just under 55% of all the $188.7 billion held by the top 50. This percentage has not changed in the last year even though $27 billion moved into this space in the last year. The bottom five managers represent less than 2% of the total with the median manager having $1.2 billion in AUM. There was only one switch in the managers in the top ten.

Our graphs list numerically the top 50 without names to focus on the structural dynamics. All the graphs are sorted largest to smallest.

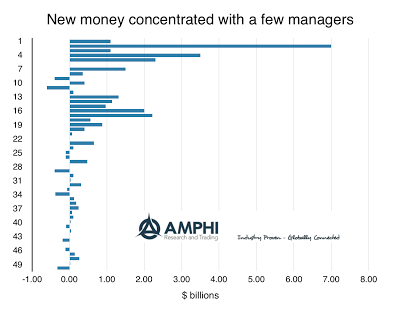

The flow of new money into managed futures was mixed but still highly concentrated. Five managers received more than their fair share, with 62% of all the new money raised, but only 2 of those managers were in the top five. “Hot” managers will get a great share of the money raised; however, a close look will not see those managers as the most recent top performers. Nevertheless, strong rolling relative performance is associated with new money flows. 11 firms lost assets over the last year.

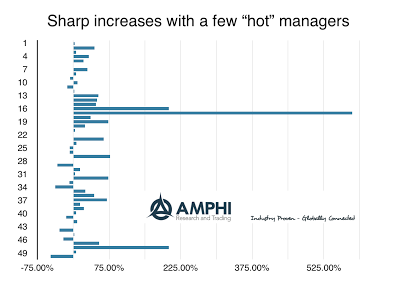

Some firms saw explosive growth in assets under management, but they were not in the top 5 or ten. The big growth was in the second quartile managers by size. 10 firms grew by more than 50% in the last year and three saw increases of more that 100%. One firm grew by more than 500%. No firm in the top 50 lost more than 50% of their assets. Investors seem willing to stay with managers and slowly leave over time while those that are perceived as winners will see money fly in.

We find those high percentage increases a concern. First, there seems to be a herding behavior by investors. Second, there is the issue of whether firms have the infrastructure to handle the strong inflows. (We plan the watch the performance of those managers who have seen the greatest growth to see if they are able to manage these tremendous inflows.)

Should we expect the numbers we see? Yes, most industries follow a power law with relatively high concentration. Given the ease of moving money and the readily available information on managers, I am a little surprised at the high concentration, but it is not unusual even in asset management. I am surprised at the high concentration of money flows to a few managers. There should be expected more flows into winners and out of underperforming managers, but these flows should be a little more disperse given volatility and market uncertainty. Given many investors will hold through a 3-year cycle, it should not be surprising that outflows are less concentrated.

It is also surprising that the median in the top 50 is only $1.2 billion. We have seen pension emerging manager programs set the criteria that managers have to be below $2 billion. By that standard only the top 20 managed futures managers would be considered beyond the emerging threshold. The standards for what is a large manager in managed futures are just not that large. Investors have to rethink what it means to be a large manager in this hedge fund space. This list certainly gives some perspective on what it means to be a big managed futures manager and how fortunes can change if you are viewed as a “hot” manager.

Related Posts

Systematic vs. Discretionary Trading: Which Strategy Is Right for Your Portfolio?

Investors face many choices when selecting investments. Historically, the main divide was between fundamental and technical trading. The growth of computer systems for trading has introduced a potentially larger variable that will only increase as AI advances, whether in systematic (rules-based) or discretionary (human judgment) trading. In just my 20 years working in the industry, […]

Bowmoor Capital – A Different Approach to Trend Following

Competing head-to-head to outsmart others doing the same strategy is often a tough road. In trend following circles, giants like Man AHL, Winton, and Aspect dominate assets under management. This enables them to hire top PhDs, deploy better technology, test ideas rapidly, and outspend smaller players on sales and marketing. So how can a smaller […]

The 6 Biggest Myths About Diversification and Non-Correlation

“If everything in your portfolio goes up and down at the same time, you have a bad portfolio.” This simple but powerful observation from Mark Rzepczynski, former CEO of John W. Henry & Company, is one I think of often – for both my customers and my own investing. A losing position in your portfolio […]