There has been a strong move to passive investing tied to benchmarks by investors. The reasons for this movement are threefold. One, passive benchmark investing is cheaper than active management. Two, active management has often underperformed benchmarks. Three, passive investing provides transparency on what will be in the portfolio. Nevertheless, a survey of defined benefit consultants suggest that the choice between active and passive management is not obvious and actually asset class specific. There are some areas where consultants view that active management is important while other areas the focus is for passive investing.

The decision between active and passive may be based on the relative efficiency of markets and the dispersion or lack of correlation across the components of the benchmark. Market inefficiencies will allow for potential profits from active management against a benchmark. Similarly, if there is less correlation within an asset class benchmark, there is likely to be fewer common factors that tie the benchmark components together in a way that would make passive investing useful. Wide return dispersion within an asset class allow for gains from picking winners and losers.

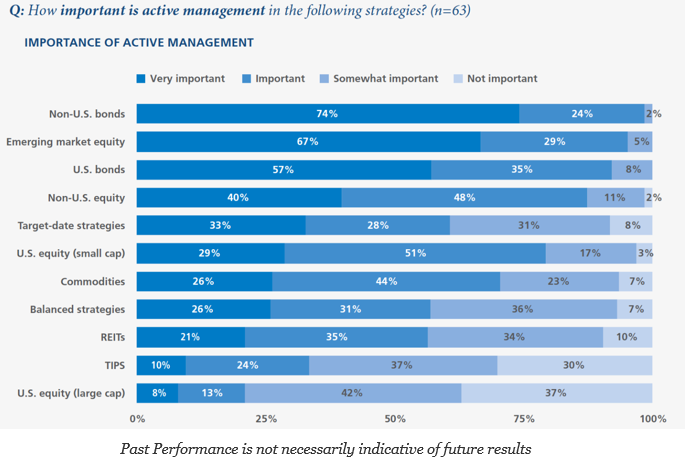

A recent survey by Pimco of Defined Contribution Support and Trends provides an interesting look into the minds of defined benefit consultants. The survey shows that for large cap equities active investing is only somewhat or not important for just under 80% of the consultants, yet active management for non-US bonds is considered important or very important for 98% of the consultants. That is a wide gap.

Non-US bonds and EM equities are very diverse, so there seems to be a reluctance to use a passive benchmark to obtain exposure in these asset classes. Large cap US equities and TIPs seem to be viewed as more homogeneous. It does seem as though DC consultants are less comfortable with passive investing regardless of the academic evidence on the skill of active managers.