The one take-away from the Great Financial Crisis has been the importance of financial intermediation, banking. When banking is disrupted, lending will not happen. There will be a cutback in credit which stalls the economy. Additionally, if capital is not available for banking, there will be a cap on lending especially if there is a constraint on leverage. Funding will become scarce. If bank capital falls, lending will be disrupted. This lending channel is amplified with the swings in the business cycle.

It does not matter whether the central bank is increasing the money supply, if financial intermediation is not occurring, there will not be economic growth. Of course, increasing money will force down interest rates, but the channels of finance need to be clear to allow the flow from lenders to borrowers.

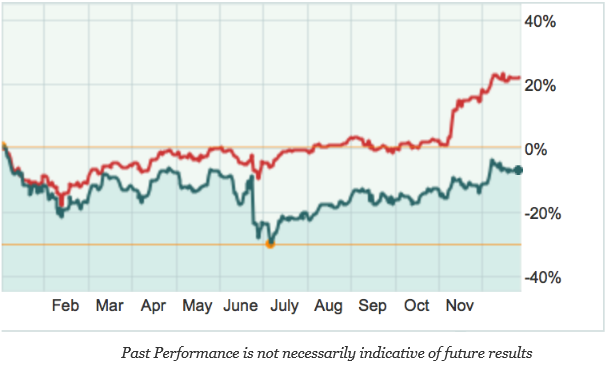

There is a large difference between the US and EU financial services indices, XLF versus EUFN, this year with close to a 25% return gap. There is the drop from BREXIT, large gain from the US election, and the risk from Italian banking which explains much of the difference. Regardless of the corporate bond purchase program of the ECB, more lending is done through banks in Europe. Poor equity performance hurts bank intermediation. This will spill-over to the rest of the economy and suggests that growth differential between the US and Europe will not be closed.