Show me the performance for the year and I should be able to tell you something about the economic and political events for the year. I may not be able to tell you the specifics, but I should tell you whether it was a “good” or “bad” year in terms of economic growth, uncertainty, risk, and confidence. Looking back over 2016, you would not know that it was a year of political upheaval.

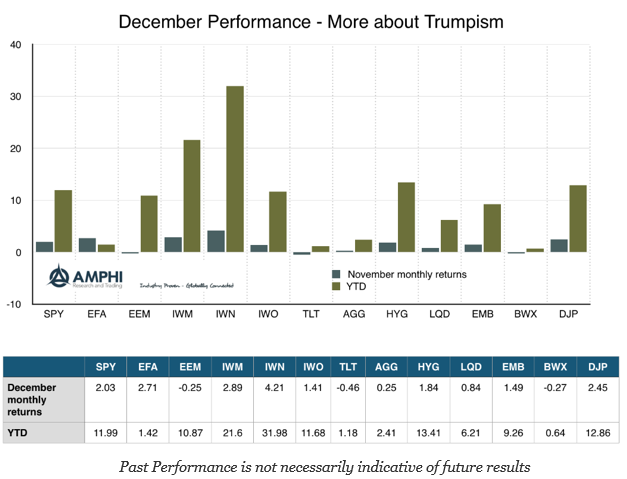

Stocks did well even after a poor first two months. Global equity markets did not share in the optimism of the US, but it was a still a positive year. The real stock gains were in small cap and value which both posted returns of over 20 and 30 percent respectively. Growth stocks also gained double digits.

Bonds generated a marginal return which suggests that economic growth is expected to be higher and inflation premiums have started to enter the market. High yield and credit index ETF’s generated superior returns which are consistent with better economic prospects. Emerging market bonds also performed well even though developed bond markets were a marginal performer.

Commodities, as measured by the Bloomberg index, posted yearly gains after a multi-year slump.

The political angst was not translated into financial markets or at least not in the form of risk-off behavior. Of course, 2017 could see something very different as the populism of 2016 is expected to be converted into macro policies in 2017.