Hedge fund managers are supposed to show skill during periods of higher risk and uncertainty. If there is more uncertainty or ambiguity concerning market, skill-based managers should be able to do better than those who just buy a market index. This is one key reason behind choosing hedge funds. When there is uncertainty and risk, alpha should be generated by skill managers.

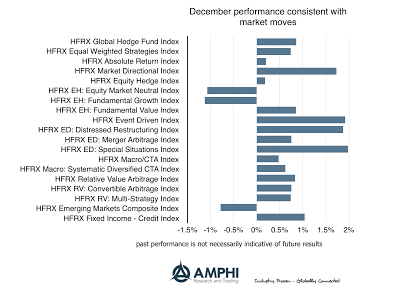

December hedge fund returns were better across the board except for market neutral and fundamental growth strategies. With strong gains in small cap and value indices, the better equity strategy returns should be expected. The special situation, event, and distressed strategies again did well to cap a strong year. Macro, fixed income, and credit also performed well this month.

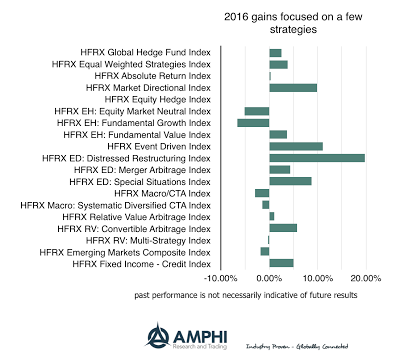

Nevertheless, the return numbers across most strategies for the year do not show strong performance. Assuming a lower beta and some alpha, most hedge funds should have been in the mid-single digits for returns. That was not the case for most strategies. Only two strategy indices generated gains greater than 10%. These two, event and distressed, are generally not tied to market moves in equities or fixed income.

Our investment premise is that skilled-based managers should do better during uncertain times. Uncertainty will likely cause less correlation and more dispersion in returns. We know that correlations go up when there are “bad” times or recessions, but when there is less clarity on market direction or on the impact of policies there is less likely to be a common factor driving returns. Those who can understand the market’s complexities should be rewarded. We expect more uncertainty in 2017, yet our confidence in hedge fund managers making money may be put to a test. Performance, not protection, is still the driver of demand for hedge funds.