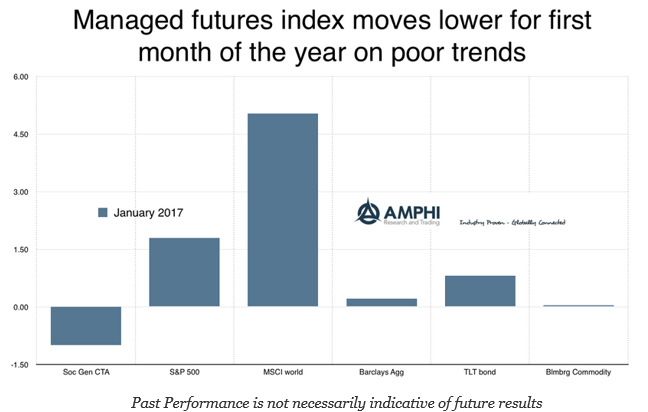

The managed futures hedge fund style, as measured by the SocGen CTA index, declined by just under one percent for the month. There was limited movement in commodities and bonds and the largest gains for the month were in non-US equities where there is usually less exposure by futures managers. Going back over our sector trend measures, we were predicting a lackluster month since there were few strong directional trends going into January. The SocGen trend indicator index was down over 6 percent and the short-term trader index declined about 4 percent.

Separating all the possible reasons for the underperformance, the cause is always simple. Most managed futures managers engage in some form of trend following or momentum trading. These managers are non-predictive in the sense that they may not have a view on the market. They are not guessing on the next market move through some fundamental framework. They look for trends to exploit and there were limited trends. You can call it signal to noise or choppiness, but opportunities did not lead to profits. No trends, no profits.

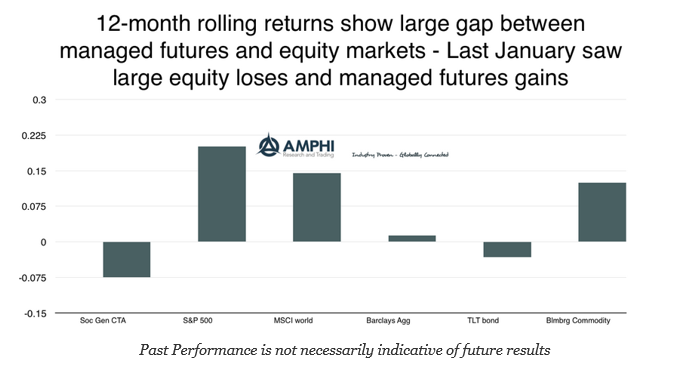

The 12-month rolling returns are negative with a large gap between managed futures returns and equities. The reason is very clear once you look at the cycle over the last year. The end of January was close to the bottom for the stock market move while managed futures posted large gains last January. With manage futures close to a peak and equities at a trough; you will get large rolling return differentials.

Related Posts

Systematic vs. Discretionary Trading: Which Strategy Is Right for Your Portfolio?

Investors face many choices when selecting investments. Historically, the main divide was between fundamental and technical trading. The growth of computer systems for trading has introduced a potentially larger variable that will only increase as AI advances, whether in systematic (rules-based) or discretionary (human judgment) trading. In just my 20 years working in the industry, […]

Bowmoor Capital – A Different Approach to Trend Following

Competing head-to-head to outsmart others doing the same strategy is often a tough road. In trend following circles, giants like Man AHL, Winton, and Aspect dominate assets under management. This enables them to hire top PhDs, deploy better technology, test ideas rapidly, and outspend smaller players on sales and marketing. So how can a smaller […]

The 6 Biggest Myths About Diversification and Non-Correlation

“If everything in your portfolio goes up and down at the same time, you have a bad portfolio.” This simple but powerful observation from Mark Rzepczynski, former CEO of John W. Henry & Company, is one I think of often – for both my customers and my own investing. A losing position in your portfolio […]