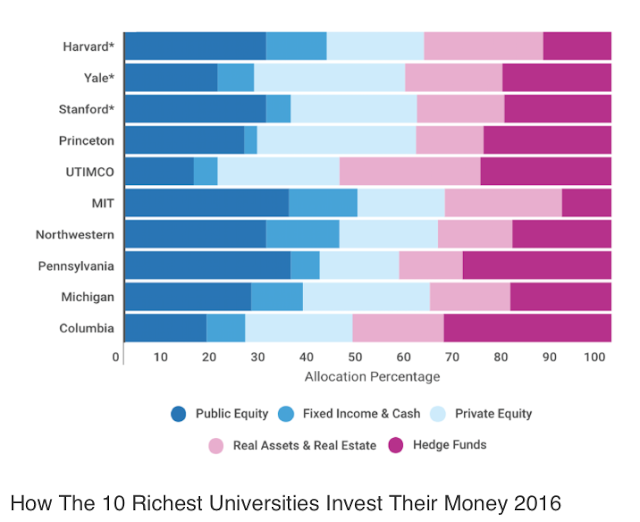

This above chart from thetrustedinsight.com provides an interesting tale about asset allocation for large endowments. Forgot about the traditional 60/40 stock/bond mix. Forget about the 50/30/20 stock/bond/alternatives mix. If you don’t need liquidity, as is the case for the endowment portfolio allocations, a mix between liquid and illiquid is a better base framework. Hold private equity and real estate as core allocations. This core is for long-term appreciation and cash flow greater than bonds, but is generally illiquid. Take money from fixed income and cash. Take funds from public equities and use hedge funds, which may have mixed liquidity, as an additional return enhancer. The public equity and bond/cash portion of portfolios is between 25 and 50%, while hedge funds are from 7.5 to 32.5% for these key endowments. The majority of their allocations are not with traditional equity and bond beta.

Making a generalization, the new endowment allocation is 35/45/20 or 35% liquid beta, 45% illiquid investments, and 20% alpha. Of course, you can come up with other descriptors given the chart numbers but we are looking for some simple commonality on the asset allocation.

First, if you don’t need the liquidity find investments that you will get paid a premium for taking on illiquidity. Second, look for alpha or return enhancements where you can find them. Hedge funds can be alpha enhancers and substitutes for fixed income or beta. Third, cut your public beta exposure or at least change it to more illiquid investments that can give more beta per dollar invested. Most private equity will be at higher market beta or credit beta.

This endowment liquidity sensitive approach is not for everyone. You have to be able to sit on investments for long periods without a need for cash and you have to have skill to find the alpha enhancers or private investment managers. Yet, it is worth thinking about how these portfolios can be replicated in a different more accessible form.