There is still concern about the potential for large moves in bonds during the next three months. The latest rolling yield changes shows a calming after the large moves late last year. Nevertheless, uncertainty on policy, growth, and the equity markets may all impact Treasury yields, the “safe” asset. If safe means limited moves in yield, investors may be in for a surprise. A flight to safety can easily take the 10-year below 2% while a pick-up in inflation or growth can lead to yields pushing closer to 3%.

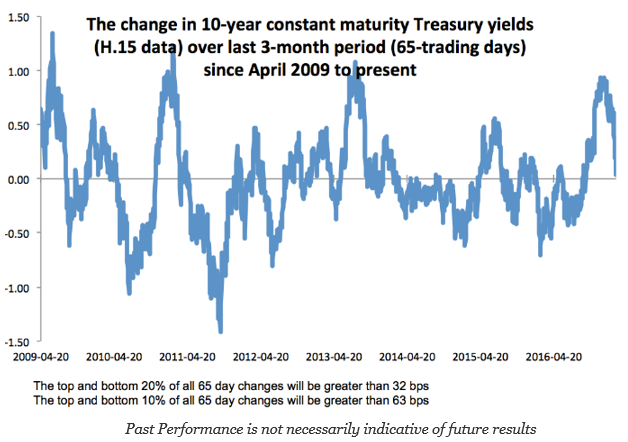

Looking at the change in yields across the post crisis periods suggests that the risks are significant just based on normal bond movements. Over any 65-day trading period for the 10-year constant maturity Treasury index there is a 20% likelihood that yields will move by more than 32 bps up or down. At the current yields, we could easily see yields above or below 2.70 and 2.10 over the next three months. More importantly, there can be a move of more than 100 bps up or down over the next quarter, albeit the probability is about 1% using data over the last seven years. What is clear is that a return to sub 2% yields or a move above 3% is not crazy talk even under a low rate environment.

After hundreds of discussions with hedge fund managers, I am still surprised that there is a fear of revealing investment processes under the assumption that someone will steal their ideas and intellectual capital. There are few investment styles that are truly unique and special. What is special is still strategy execution – the practical process of delivering returns. Skill is with the decision-making execution of information and strategy.

All hedge funds are not created equal as the return box chart shows for the post Financial Crisis period. There is a significant amount of dispersion across hedge fund styles. Over the period 2009-2018, the difference between the best and worst hedge fund category is almost 7 percent after we account for global equities and bonds.

The attraction to private equity and other less liquid alternatives is clear from the Guide to Alternatives by JP Morgan Asset Management. The return profile is much higher for private equity and debt funds than more liquid alternatives and global bonds; however, the dispersion in returns is multiples higher than what can be expected from other public categories.