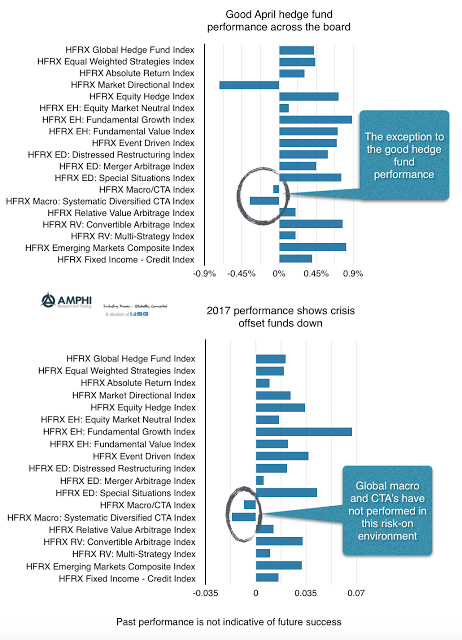

No hedge fund strategy will make money all of the time. As the market and economic environment changes, the performance of different strategies will also change. Hedge fund factor exposures will be different based on the strategy employed by the manager. If you cannot predict the environment factor exposures, there is value with holding a diversified portfolio of hedge funds. April performance clearly shows the difference in strategy behavior.

We are in a risk-on environment. Hence, those strategies that do well in “bad times” or risk-off regimes will underperform other hedge fund strategies. We should not be surprised by the current macro/systematic/CTA performance. We may not like it, but it is within some tolerance of expectations.

Given the average beta for many equity hedge fund strategies, performance is within expectations. Long-only hedge positioning should do better in a reflation environment. We may expect better alpha generation; however, the low volatility regime may limit the set of opportunities for stock-picking or relative value trades.

After hundreds of discussions with hedge fund managers, I am still surprised that there is a fear of revealing investment processes under the assumption that someone will steal their ideas and intellectual capital. There are few investment styles that are truly unique and special. What is special is still strategy execution – the practical process of delivering returns. Skill is with the decision-making execution of information and strategy.

All hedge funds are not created equal as the return box chart shows for the post Financial Crisis period. There is a significant amount of dispersion across hedge fund styles. Over the period 2009-2018, the difference between the best and worst hedge fund category is almost 7 percent after we account for global equities and bonds.

The attraction to private equity and other less liquid alternatives is clear from the Guide to Alternatives by JP Morgan Asset Management. The return profile is much higher for private equity and debt funds than more liquid alternatives and global bonds; however, the dispersion in returns is multiples higher than what can be expected from other public categories.