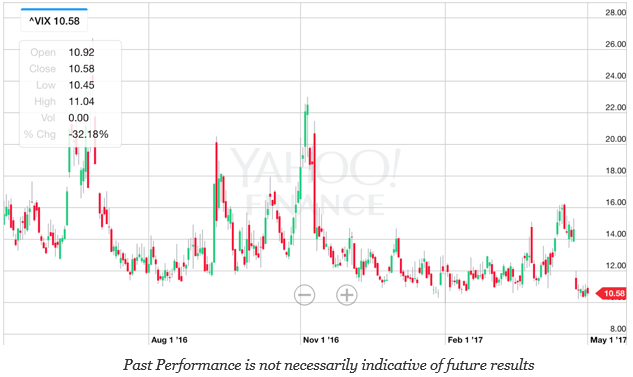

The VIX index, the most widely watched measure of market volatility, is at extended lows with a jump lower after the French presidential first round election results. The uncertainty and risk premium from this election has been taken out of the market. Economic uncertainty has also fallen since the US election although it is still elevated since the earlier last fall.

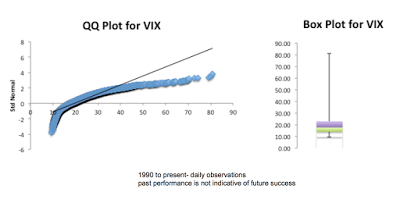

Is volatility a thing of the past? Well, it seems that way. We looked at close to 7000 daily quotes on the VIX since 1990 and found that current volatility is at the 1.45 percentile. It is low. These low values do not last, but any strategy that needs a spread in the distribution will not do well during these periods.

It should be noted from the QQ plot and the box plot that the distribution of volatility is far from normal. So even though volatility is low, the weight of the distribution is skewed to values below 20. This is not a normal distribution but one with significant positive skew.

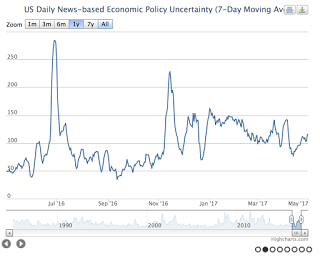

The question in not whether the VIX will change, but rather how long will the low volatility persist. The policy uncertainty index has fallen since the Brexit and election highs over the last year, but it is not at significant lows. The latest GDP numbers for the first quarter are lower than expected. Lower end economic performance usually is associated with higher volatility.

Given the distribution of VIX prices, a comparison of toady’s level versus the level in a month or two would not be helpful. Mean reversion will occur; nevertheless, the extent of the move may be limited given the clustering of low VIX values. There is a 32% chance of the VIX being below 15; a 50% chance below 18; and a 62% chance below 20.

The big move event is not likely if you are playing the odds. The numbers shows that upside jumps in the VIX are more likely than downside spikes. There is nothing usual with this behavior, but over any twenty day periods, there is only a 5% chance of jumping by more than 7 vol points and only a 4.75% chance of seeing a 40% or better up move over any 20-day period. Anyone expecting a big vol jump on mean reversion will be disappointed. This would still mean a vol that is less than 20 in the next month even if we had a significant spike.

We are not saying to accept low vol as a part of everyday life, but a return to anything like behavior during the Financial Crisis is unlikely.

Related Posts

Anatomy of a Tough Month for Trend-Followers: Tariff Shocks & Volatility Spikes

It is often said that trend followers provide “crisis alpha.” This means that market stress often benefits their strategies. This follows logically as moves get larger, coordinate together, and run consistently, trading becomes easier. These managers quickly caution that they do not always provide this negative correlation. Price action can swing unpredictably against long-standing trends […]

Time-varying correlation – Diversification benefits are dynamic

What is the correlation between two assets? The correlation is critical because it is the driver for any diversification decision. The better question is, “What is the correlation now, and what can it be in the future?”. Correlations are often time varying and regime specific. In bad times, correlations rise, so the diversification expected is not present when you need it. This phenomenon requires more thinking about tail risks and how to best address them.

The “3 by 5 Index Card” on What You Need to Know About the February VIX Spike

University of Chicago professor Harold Pollack in an interview a few years ago mentioned that the best money advice can fit on a three-by-five inch index card. He was then challenged to write the card. His financial advice went viral. We follow this tradition by focusing on a simple “three-by-five index card” on the VIX volatility spike earlier the month.