Here is a simple question that should have an easy answer. Name a universal set of asset classes that can be employed to categorize the investments for a large university endowment. The answer to this question may astound you. There is no agreement on the number of asset classes an endowment should have in order to make asset allocation decisions. That’s right, the largest university endowments cannot agree on this basic number for how to categorize investments. See the paper, “The evolution of asset classes: Lessons from university endowments”, Journal of Investment Consulting Vol 17, no 2, 2016.

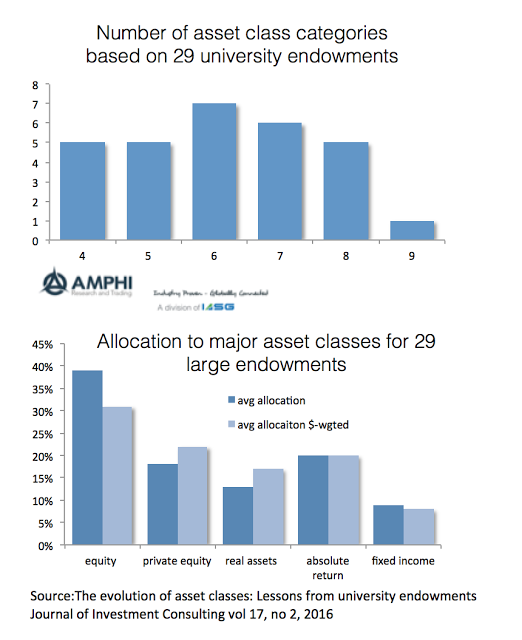

The median number of categories for a group of leading endowments surveyed in the article is 6 with a maximum number of 9 and a minimum number of 4. This breakdown is for a set of 29 as shown in the figures below that represent just over half of the endowments included in the research study. With all of the education and discussion about the simple question of how you should bucket securities to make asset allocation decisions, some of the largest university endowments show no commonality concerning this number. However, this just scratches the surface with many other endowments producing deeper granularity and other universities forsaking asset classes and focusing on factors and asset classes.

An asset class should have some simple characteristics. It should be definable, have something that can serve as a benchmark, be uncorrelated with other asset classes, and understandable. Even this simple categorization can lead to arguments. Are international equities a separate asset class? What about private equity? What about emerging markets or hedge funds that focus on equities? If we move to fixed income, there are simple questions of whether government bonds should be separate from credit. Is cash different than bonds? Should real estate and commodities be separate or combined as a real assets? The question of how to divide hedge funds is another definitional trap. How many hedge fund categories are appropriate? Many focus on long/short equity and all else.

The impact of these choices is real especially with less exposure focused on equities and fixed income. If asset allocation decisions and performance monitoring is to be done effectively, it seems such a simple question as setting the right buckets should be universally addressed. Are more categories better than less? Of course, the real issue is whether this should matter. If I have fewer or more categories for classification will this help generate better performance? That critical issue still needs to be answered.