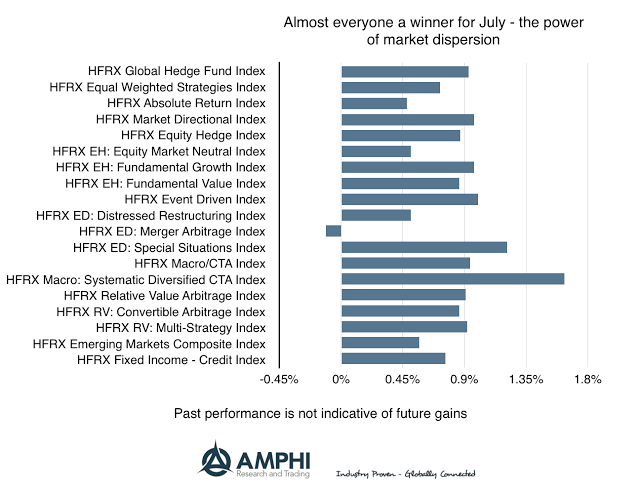

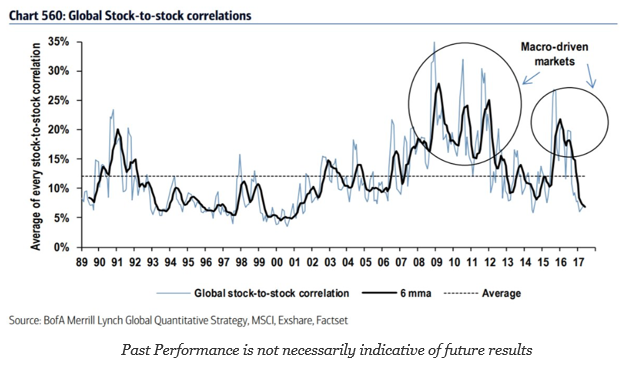

Almost all HFR hedge fund strategy indices were positive for the month of July. In many cases, the strategies beat small cap and value indices for the month. Our take on this good performance is that the increased dispersion in returns, lower average correlation across equity pairs, is a key reason for the gains. Greater dispersion means there are greater opportunities for stock pickers to differentiate themselves.

The stronger macro returns were based on the strong dollar decline and selected cross-market opportunities along with the upward movement in stocks around the world.

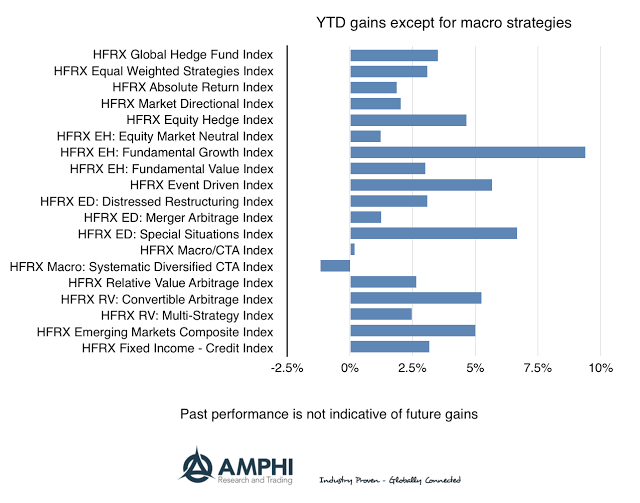

All hedge fund strategies except for systematic CTA’s have moved into positive territory for the year; however, alpha production for the first seven months seems limited relative to broad benchmarks and historical beta exposures.

The true test of hedge fund value may be seen in the next five months. If market indices decline, the expectation is that hedge funds will be able to minimize their beta exposures. If the upward trends continue with further return dispersion, we expect that hedge funds may increase their absolute return and alpha production. Hence, the value of hedge fund will be shown through their ability to provide diversification benefit in both up and down markets.