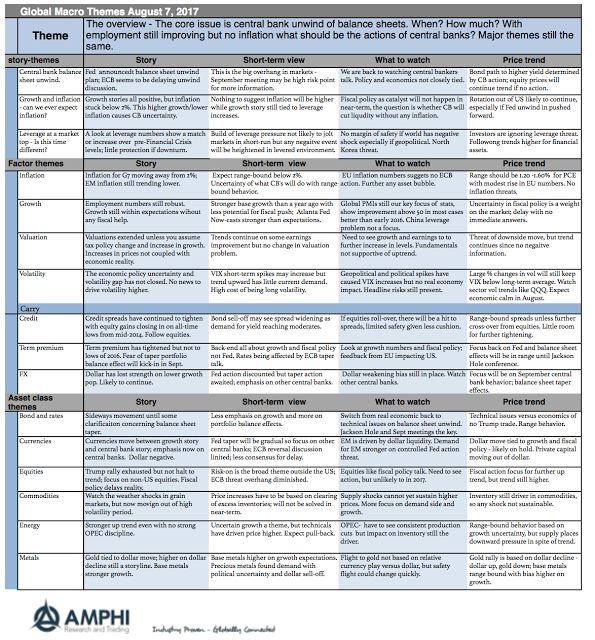

How often are we going to hear about the overvaluation in equity markets? It already seems too much, yet talk is cheap because markets continue to trend higher. The focus should be on what events will cause this trend to reverse; nevertheless, a trend in place will stay in place until there is a reason to change. Unfortunately, a change in a trend usually comes from a surprise.

We have not adjusted significantly the story-themes from last month. In fact, themes usually last for months, so this is not unusual. There are only two major themes that should be the focus of investors. One, the timing for when the Fed will start the balance sheet tapering. The market has been given details. The Fed wants investors to prepare for it. Unfortunately, many investors have not focused on these details and the implications of balance sheet reversals. As these implications sinks into investor expectations, we expect a change in risk sentiment. Two, the current leverage around the world cannot be sustained. Many economies are at or above Financial Crisis levels. Of course, the ability to pay for this debt is stronger given the low interest rates, but the current rate environment cannot give any further market relief. There will a catalyst for a deleveraging event, and when that happens, asset prices will reverse.

We expect that balance sheet tapering may be the catalyst for a deleveraging event. This is not an August event, but more likely to come to a head during fall central bank meetings.

Related Posts

Decoding Metals Price Action

Markets often communicate more clearly through price action than through headlines. The dramatic surge in metals contracts is sending a powerful signal, but what exactly is it telling us? Traders frequently monitor inter-market relationships for early warnings. When one asset class moves unusually, it can ripple across the system or reveal deeper structural issues. In […]

2025 in Review: Markets, Policy, and the Path Forward

History never repeats itself, but it often rhymes. This is even more so the case this year, as Trump began his second term with similar but different disruptions to the markets. Rising stocks, normalizing inflation, and the AI boom took center stage. We discuss some of the key events below and try to anticipate where […]

The Bankruptcy Cycle Returns: Delayed Failures and the Cost of Easy Money

Proper forest management requires clearing dead brush, protecting high-risk areas, and conducting controlled burns. As January 2026 approaches, marking the one-year anniversary of the devastating Southern California wildfires that destroyed over 16,000 structures, we examine the mistakes made and how those lessons apply to the financial markets. Much like forest fires, risk can be mitigated […]