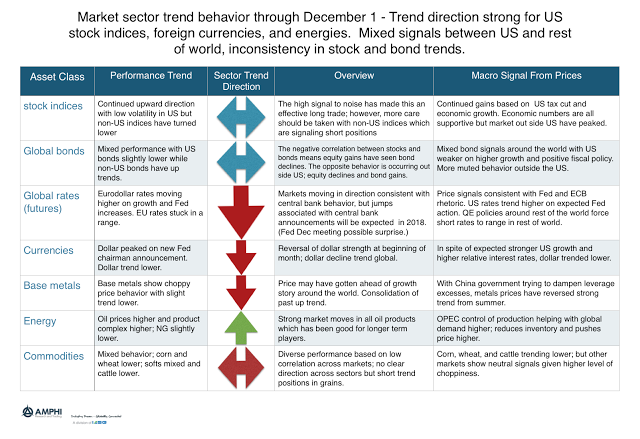

Trend behavior last month was mixed for many CTA managers. The allocation weights had a significant impact on November performance. We believe there may again be significant dispersion in performance because trend dispersion is high. For example, US stock indices show strong up trend signals while non-US stock indices are showing clear short signals. The opposite is the case for bonds where US bond signals are for short positions while non-US bonds signals point to long positions.

The dollar reversed long signals and is now showing sell signals on lower prices in spite of higher interest rates versus other developed countries, tighter monetary policy and higher economic growth signals. The oil complex continues to produce long signals. Base metals have generally been choppy but now have a short bias. Commodities do not have clear signals expect for down trends in corn and wheat.

After hundreds of discussions with hedge fund managers, I am still surprised that there is a fear of revealing investment processes under the assumption that someone will steal their ideas and intellectual capital. There are few investment styles that are truly unique and special. What is special is still strategy execution – the practical process of delivering returns. Skill is with the decision-making execution of information and strategy.

All hedge funds are not created equal as the return box chart shows for the post Financial Crisis period. There is a significant amount of dispersion across hedge fund styles. Over the period 2009-2018, the difference between the best and worst hedge fund category is almost 7 percent after we account for global equities and bonds.

The attraction to private equity and other less liquid alternatives is clear from the Guide to Alternatives by JP Morgan Asset Management. The return profile is much higher for private equity and debt funds than more liquid alternatives and global bonds; however, the dispersion in returns is multiples higher than what can be expected from other public categories.