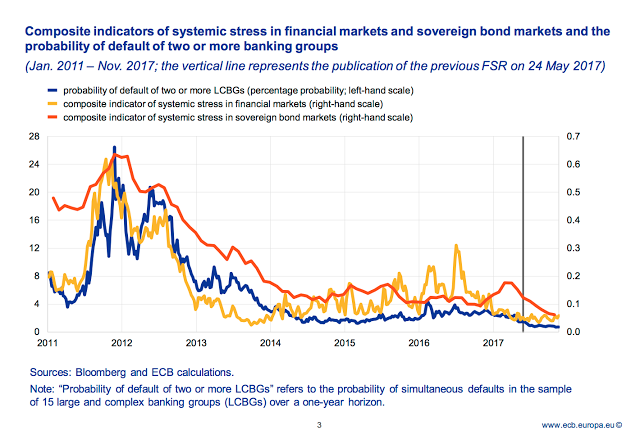

“Risk of a rapid repricing in global markets”; this ECB quote was a key talking point in the press release from the ECB Financial Stability Report issued last week. Note that “rapid repricing” is a polite way of saying asset price declines.

A close review of the ECB FSR data shows, however, that the financial environment is actually quite good. The central bankers are drawing their conclusion based on a simplistic idea of mean reversion; the more the environment looks stable and asset prices rise, the more likely there will be greater future risks.

That may be true and we find this narrative compelling, but like many forecasters, you can be right about the event or right about the timing but you are unlikely to be right about both. Without a story about when repricing will occur, the ECB’s assertion is without much value.

Nevertheless, investors should build their portfolios to have a contingency against rapid repricing.

Given that a repricing event may also include an increase in correlations to one, strategy diversification not just asset class diversification is an important tool for portfolio protection. This idea of portfolio protection through strategy diversification is why portfolio construction should be in the BAG through focused management of Beta, Alpha, and Gamma.

An investor should construct a portfolio to address these three issues:

- What is the portfolio beta desired?

- Where is the portfolio generating alpha?

- What strategies will produce gamma or positive convexity?

Portfolio beta can be changed to reflect relative desire for risk. Alpha can be found through looking for unique strategies and manager skill. Portfolio gamma usually will not come from an asset class, so active strategies like trend-following are needed for creating dynamic sensitivities to market beta. The portfolio gamma comes from a macro strategy that will increase asset class exposure to winner and decrease exposure to losers. This is the managed futures trend-following story.

Think about what is your portfolio BAG.

See,

What you need to BAG performance – Beta, Alpha, Gamma