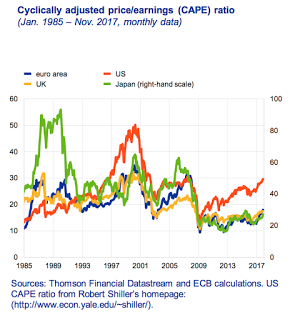

The talk has focused on the overvaluation and “bubble” with US stocks, but there are other relative opportunities in risky equity assets. A comparison of CAPE across the world shows that the UK, euro area, and Japan valuations are closely tied together, significantly below highs from 2008, and all relatively cheap versus US.

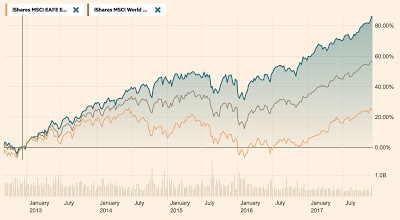

Note that if we compare the SPY versus MSCI EAFA and MSCI world indices, there is the same directional pattern but not the same magnitude of gains. The gain in favor of the US over 5 years is respectively close to 25% and approximately 60%.

International diversification has been a drag on equity performance for many investors, but now on a valuation basis, this diversification may provide upside potential and some potential muting of a US market decline.

After hundreds of discussions with hedge fund managers, I am still surprised that there is a fear of revealing investment processes under the assumption that someone will steal their ideas and intellectual capital. There are few investment styles that are truly unique and special. What is special is still strategy execution – the practical process of delivering returns. Skill is with the decision-making execution of information and strategy.

All hedge funds are not created equal as the return box chart shows for the post Financial Crisis period. There is a significant amount of dispersion across hedge fund styles. Over the period 2009-2018, the difference between the best and worst hedge fund category is almost 7 percent after we account for global equities and bonds.

The attraction to private equity and other less liquid alternatives is clear from the Guide to Alternatives by JP Morgan Asset Management. The return profile is much higher for private equity and debt funds than more liquid alternatives and global bonds; however, the dispersion in returns is multiples higher than what can be expected from other public categories.