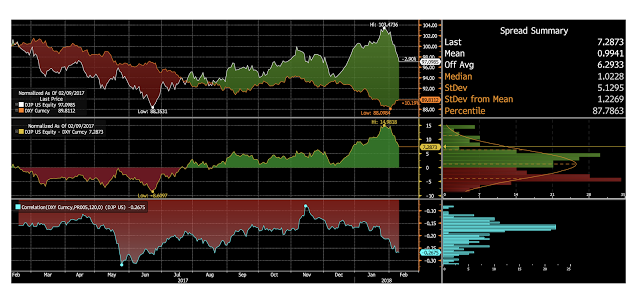

The dollar may be trending down, but investors should also look at the second order effects of what will happen to other markets. For example, a declining dollar is good for long commodity exposure. The long commodity argument is twofold, one, a decline in the dollar makes commodities denominated in dollars cheaper to foreign buyers which will increase demand; two, a decline in the dollar associated with global growth will increase global commodity demand. There are both substitution and income effects.

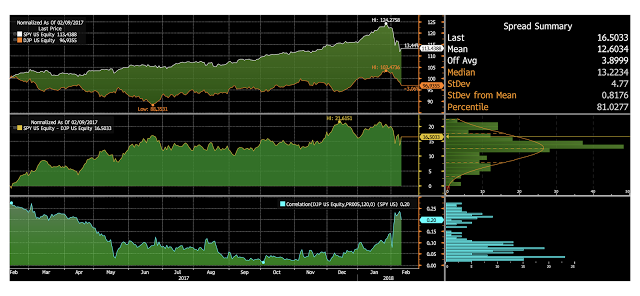

Now, a dollar decrease will make producer prices for commodities in the US more expensive but the size of the US economy and the demand for raw commodities is falling relative to the rest of the world so this dollar-commodity effect will be stronger as the rest of the world gets larger versus the US.

The dollar link will not be the only driver, but for longer-term asset allocation, it a good relationship that can be exploited. Additionally, the correlation between stocks and commodities is low, so investors gain diversification from holding commodities at a time when they are cheap relative to finical assets and there are higher expectations for inflation.

Related Posts

Race to Nowhere: Markets Pause Before the Next Big Move

Running on a treadmill is one of my least favorite activities: you expend a lot of energy but end up exactly where you started, only out of breath. So far in 2026, financial markets are behaving similarly. There’s intense activity, but the major indices have gone almost nowhere. As of mid-February, the S&P 500 is […]

Decoding Metals Price Action

Markets often communicate more clearly through price action than through headlines. The dramatic surge in metals contracts is sending a powerful signal, but what exactly is it telling us? Traders frequently monitor inter-market relationships for early warnings. When one asset class moves unusually, it can ripple across the system or reveal deeper structural issues. In […]

Gold’s Resurgence: Can Crypto Really Replace the Yellow Metal?

Once left for dead, gold speculators can sleep easily in 2025 as the yellow metal sits at all-time highs once again. Despite the shift to Bitcoin and other digital assets, the enduring nature of gold as an inflation hedge continues. What is driving this surge, and will cryptocurrencies still win the battle? Reasons for optimism […]