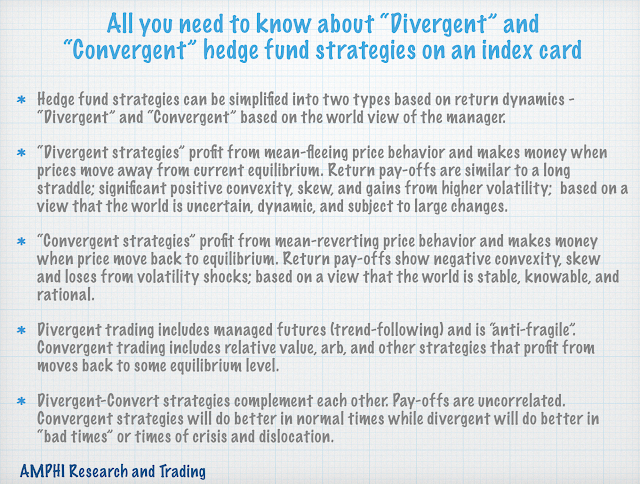

This is the second in our series; all you need to know about a topic should fit on a “3 by 5” index card. We think the complexity of hedge fund investing can be simplified if the simple dichotomy of divergent and convergent trading is used as a primary method of describing potential return pay-offs.

If you strip away all of the activities and the just get down to basics, strategies are based on the world view of the manager and will either make money when prices move away from the mean or equilibrium price or prices revert to the mean or equilibrium price. If a manager believes the world is knowable, stable, and rational, he will be comfortable taking relative value arbitrage risks. If a manager believes the world its unknowable, dynamic, and subject to mistakes and biases, he will be comfortable with strategies that make money from market dislocations.

Investors will be rewarded from convergent trading when prices are stable and times are normal. You will be rewarded with holding divergent strategies when there are large market dislocation and price movement away from the mean. This is not the end of the story on hedge fund investing but a good start for any discussion.

After hundreds of discussions with hedge fund managers, I am still surprised that there is a fear of revealing investment processes under the assumption that someone will steal their ideas and intellectual capital. There are few investment styles that are truly unique and special. What is special is still strategy execution – the practical process of delivering returns. Skill is with the decision-making execution of information and strategy.

All hedge funds are not created equal as the return box chart shows for the post Financial Crisis period. There is a significant amount of dispersion across hedge fund styles. Over the period 2009-2018, the difference between the best and worst hedge fund category is almost 7 percent after we account for global equities and bonds.

The attraction to private equity and other less liquid alternatives is clear from the Guide to Alternatives by JP Morgan Asset Management. The return profile is much higher for private equity and debt funds than more liquid alternatives and global bonds; however, the dispersion in returns is multiples higher than what can be expected from other public categories.